BCW 38: Spotify

A case study in unit-economics endurance and the patience of the company that took 18 years to make money

Welcome to our 34 new readers & followers

Earlier this month I read Spotify’s Q1 2026 numbers. 761 million monthly users. 293 million paid subscribers. €715 million in quarterly operating profit on €4.5 billion of revenue. A Q1 free cash flow record of €824 million [1].

Daniel Ek had been gone from the CEO chair for exactly four months. He stepped aside on January 1, 2026, right after the company posted its first full year of profitability in 18 years of operation [2][3].

He stayed long enough to see one clean profitable year, and then handed the keys to two co-CEOs to focus on Helsing, the German military-AI drone company he chairs [4].

For 18 years Spotify ran a structurally broken P&L. The recorded-music labels took roughly 70 cents of every premium dollar before the company spent a single euro on engineering, marketing, content, hosting, or anything else [5]. And the only thing holding the company together through that gap was a founder willing to keep saying it would work.

From a builder’s standpoint the interesting thing about Spotify is not that it became the world’s largest music streamer. It is that the team figured out how to bolt a high-margin business (podcasts, audiobooks, fitness, ads) on top of a low-margin one (licensed music), and used the first to subsidize the second long enough to win the market.

A Stockholm Apartment, 2006-2008

In the autumn of 2006, on the second floor of an apartment building on Riddargatan, in the part of central Stockholm where the business district meets the residential streets of Östermalm, a handful of KTH engineering graduates spent their first week lugging IKEA flat-packs up the stairs and assembling office furniture [6]. They unpacked whiteboards. They installed servers. They built their company’s first headquarters out of a residential apartment because they could not yet afford anything else.

Among them was Daniel Ek, twenty-three years old, fresh out of a personal collapse he would later describe in interviews as a period of depression after selling his first company. Beside him, on paper at least, was Martin Lorentzon, the older, wealthier co-founder who had just committed roughly €1 million in seed money out of his own pocket and resigned publicly from TradeDoubler, the affiliate-marketing company he had taken public a year earlier [7].

Daniel Ek grew up in Rågsved, a working-class district south of Stockholm, raised mostly by his mother and stepfather [8]. He started building websites for local businesses at thirteen and, by his own account, was charging up to $5,000 per page and clearing close to $50,000 in some months from a computer in his bedroom [9].

He dropped out of KTH Royal Institute of Technology, founded an online-ad company called Advertigo, and sold it to TradeDoubler in March 2006 for roughly $1.25 million. He was 23. He bought a red Ferrari, a luxe central-Stockholm apartment, and tried to retire into nightlife [9][10]. The retirement lasted only a few months. By the summer of 2006 he had moved into a cabin in the woods, sold the Ferrari, and was, in his own description, fumbling for a purpose [11].

The idea that pulled him out was specific. Napster, the file-sharing service that had taught a generation of listeners to expect any song instantly and for free, had collapsed in 2002 under lawsuits. Apple’s iTunes Store had become the legal alternative, but only by reinstating ownership and price-per-track in a market the pirates had already trained to want neither [12]. Ek and Lorentzon’s bet was that the answer was not to make people pay per download. It was to make piracy obsolete by offering something better than piracy.

I realized that you can never legislate away from piracy.

Daniel Ek, paraphrased from his 2017 reflection on Spotify’s origin thesis, in Frederick AI founder profile [12]

Lorentzon’s first $1 million in seed funding bought roughly two years of runway [13]. The team spent it on two things in parallel. First, they engineered a desktop client whose key feature was sub-200-millisecond start-of-play time so that streaming would feel like local playback. Second, they took on the substantially harder problem of getting the four major music labels (Universal, Sony BMG, Warner, EMI) to license their catalogs at all [13][14].

Industry observers at the time would have called the licensing path naive. The labels had killed Napster, MyMP3.com, Grokster, and Kazaa through litigation. They had given Apple a per-track download model precisely because they did not believe streaming would generate enough money to compensate for the loss of ownership economics. The conservative move for two Swedish founders with a million euros was to license their software to an incumbent, build a small ad-supported product in Scandinavia only, or pivot to something Apple was not already winning. Ek refused. He spent two years in licensing negotiations, eventually structuring deals in which the major labels received not just royalties but equity in Spotify itself. That structure gave the labels long-term upside and gave Spotify a permanent cost-of-goods problem [15][16]. After raising a $21.6 million Series A in 2008, the team launched Spotify on October 7, 2008, by invitation only, in the United Kingdom, France, Spain, and the Nordic markets [3][14].

Active learning question. You are Lorentzon in mid-2007, eighteen months into licensing talks with Universal and Warner, with your seed capital running low and no signed deal in any major market. The labels are using the threat of walking away to push for higher advances and equity. Do you keep negotiating, license to a smaller catalog and launch with what you have, or pivot to a model the labels cannot block? What changes in your reasoning if you know that the labels’ counter-offer has gone from rejecting your model to demanding 6-7% equity in your company?

The Sean Parker Email and the American Crossing, 2009-2014

Spotify launched in Europe in October 2008 with two products that almost no streaming competitor had bothered to combine.

An ad-supported free tier with no time limits. And a premium tier at €9.99 per month with no ads and offline playback. By the end of 2010 it had grown past 10 million European users and an unrepeatable piece of intellectual property: a freemium funnel that converted heavy free listeners into paying subscribers at a rate that, in some Scandinavian markets, ran north of 20%. Nobody in the United States believed those numbers were possible [18]. The conventional wisdom in San Francisco was that free listeners would never pay if they did not have to. Spotify’s data said the opposite. The free tier was the most powerful conversion engine the music industry had ever had, because it broke the inertia of piracy first and asked for the credit card second.

On August 25, 2009, Sean Parker, the Napster co-founder turned Facebook’s first president turned Founders Fund partner, sent Ek an unsolicited email. Spotify had been recommended to him by, of all people, Mark Zuckerberg, whom Parker had been pestering for months to look at the Swedish service [19][20].

I’ve been playing around with Spotify. You’ve built an amazing experience.

Sean Parker, email to Daniel Ek, August 25, 2009 [19]

The Parker introduction mattered because it solved the second-hardest problem after licensing: relationships with the American labels. In 2010 Parker’s Founders Fund led a $15 million round, Parker joined Spotify’s board, and he personally negotiated terms with Warner and Universal Music Group [20][21]. On July 14, 2011, Spotify launched in the United States. Within six months it had crossed 5 million U.S. users [22].

Between 2011 and 2014 Spotify did two structurally important things beyond geography. First, it built a mobile product. In September 2009 it had launched iOS and Android apps. Uniquely among streaming products at the time, they let Premium subscribers cache tracks for offline listening, turning a desktop service into a phone-first one before the iPhone had displaced PCs as the primary music device [24]. Second, in March 2014, it acquired The Echo Nest, a music-intelligence company spun out of the MIT Media Lab. Its algorithms parsed both audio (tempo, key, instrumentation, “danceability”) and metadata (genres, artist descriptors scraped from music journalism) into a vector representation per song [25].

Without Echo Nest, Spotify’s recommendation engine was collaborative filtering, which is recommendation by user-behavior overlap, the same trick Amazon had used since the 1990s. With Echo Nest, Spotify could mix collaborative filtering with content-based features and natural-language processing of how critics described music, producing recommendations that felt like a friend’s mixtape.

Active learning question. You are Parker on Spotify’s board in late 2010, deciding whether to push for a U.S. launch in 2011 or wait until 2013. The labels are signaling cooperation but want higher advances. Apple has just acquired Lala but not launched a streaming product. Pandora is preparing to IPO at a $2.6 billion valuation. What is the cost of waiting two years, and what is the cost of moving too early before you have the consumer side built out in the U.S.? Which would you optimize for, and how would you defend that call to a board that has already burned three years on licensing negotiations?

Becoming an Audio Platform, 2015-2020

Discover Weekly, Spotify’s most copied product feature of the past decade, started as a Hack Week project given to a small engineering team in 2014 and shipped on a Monday in July 2015 [25][26]. Each user received a 30-song personalized playlist every Monday morning, generated by combining the Echo Nest’s content vectors with collaborative filtering across the listening patterns of Spotify’s then 75 million monthly users. Within six months, more than 40 million Spotify users had streamed at least one Discover Weekly track [27].

Ek would later admit that he himself did not initially understand why this single feature would matter so much [28]. What it did, in practice, was move Spotify from being a catalog (which any competitor could license) to being a recommendation engine (which required years of training data). The asymmetry between a commoditized catalog and a proprietary recommendation layer is the moat that the entire personalization industry has tried to replicate since.

In February 2019, Spotify announced acquisitions of Gimlet Media (a premium podcast studio) and Anchor (a podcast hosting and creation tool), and committed to spending up to $500 million on podcast acquisitions that year [31]. Ek’s analysis was structural. Music had locked-in 70-cent-on-the-dollar cost of revenue because of the label royalty agreements, and no amount of scale would compress that ratio. Podcasts, by contrast, were a content category Spotify could own (through exclusive licensing and acquired studios), with fixed-cost rather than variable-cost economics. Every additional listener of a podcast Spotify already owned was nearly pure margin.

The most public expression of this thesis came on May 19, 2020. Spotify announced an exclusive licensing deal with Joe Rogan, the comedian-turned-podcaster whose show was, even then, the largest podcast in the world. By 2022 the New York Times confirmed the true value was at least $200 million over three and a half years [32]. The bet was that Spotify could move heavy listeners of the single most popular show in audio into the Spotify app, capture their attention against music streams, and use the data to build podcast-advertising infrastructure that Apple, which had a market-leading podcast catalog but virtually no native monetization, would not match.

The steelman alternative at the time was clear and was articulated by several outside analysts. Concentrating $200 million on a single creator was the precise inverse of the catalog-distribution model Spotify had built in music. It created key-person risk, brand-association risk, and a precedent that would force Spotify into a permanent escalating bidding war for premium creators. The case for spreading $200 million across a portfolio of fifty studios and 1,000 creators was, on paper, the rational version of the same bet with lower variance. What changed in Ek’s thinking was that he believed the listener data alone, the cohort of Rogan’s millions of weekly listeners now inside the Spotify app, attributable and behaviorally trackable, was worth the price independent of Rogan’s content [28]. Within eighteen months that thesis would be tested in the worst possible way.

Active learning question. You are Ek’s CFO in early 2020, weighing the Rogan deal. The financial math says Rogan brings roughly 11 million weekly listeners, of whom you estimate 30-40% are likely to be new Spotify accounts. Each listener is worth approximately $X in advertising over three years. The deal pays $200 million. The brand and concentration risk is real. What internal threshold would you require (minimum listener migration, minimum content-moderation cost cap, minimum termination clause) before recommending the deal to the board? Would you do the deal at all?

The Cost of Being Right, 2021-2024

In late January 2022, Neil Young, the 76-year-old Canadian folk-rock musician, posted an open letter on his website demanding Spotify choose between his music and Joe Rogan, whose show had been hosting guests promoting unproven COVID-19 treatments and questioning vaccine safety. Within a week, Young’s catalog was off the platform, and Joni Mitchell, Graham Nash, David Crosby, and India Arie had followed [33][34]. A coalition of 270 physicians and scientists had earlier signed an open letter to Spotify calling the show’s content objectionable and offensive misinformation [33]. Then, shortly after, a compilation video surfaced of Rogan using racial slurs across past episodes, prompting Spotify to pull approximately 70 episodes from the archive at Rogan’s own request [33].

Ek’s response, communicated in an internal staff memo and a public blog post, was to add content advisories to COVID-19-related podcast episodes, commit $100 million to creators from historically marginalized backgrounds, and decline to remove Rogan. The bet was that the controversy was a brand cost, not a business cost. The listeners who would leave Spotify over Rogan were a small fraction of the listeners Rogan brought in. Rogan himself later claimed on his show that he had added two million subscribers during the height of the controversy [35]. In February 2024, Spotify signed Rogan to a new multi-year deal reported at $250 million and ended his exclusivity, restoring the show to Apple Podcasts and YouTube [36].

A second-order win arrived on March 4, 2024, when the European Commission fined Apple €1.84 billion for abusing its dominant position in music streaming through App Store anti-steering provisions, rules that had prevented Spotify and other developers from telling iOS users about cheaper subscription options available on the open web [42]. The complaint that triggered the investigation had been filed by Spotify in 2019. Ek’s public response was characteristic. Rather than celebrate, he posted a video saying Apple was trying to seal off the open web inside its own walls [43].

The internet is at risk.

Daniel Ek, video statement on X following the EU Commission’s Apple ruling, March 4, 2024 [43]

Active learning question. You are Spotify’s head of content policy in February 2022. Neil Young has just pulled his music. The doctors’ letter has 270 signatures. Internal data shows Rogan listeners convert to Premium at roughly 1.5x the platform average and have meaningfully higher engagement on ads. The brand-research team has surveyed lapsed users and found the controversy has measurable but limited impact (single-digit-percentage exits among 18-29-year-olds in urban U.S. markets). What is your recommendation to Ek, and what are the three metrics you would track over the next 90 days to know whether your recommendation was right?

The Founder Steps Aside, 2025-2026

By the second half of 2025 Spotify had become two stories at the same time. The financial one was clean: 696 million users, €4.2 billion in Q2 revenue, the company’s first full year of profitability in its rear-view, and a stock that had appreciated roughly 6x from its early-2023 lows [44]. The political one was messier. In June 2025, Daniel Ek’s investment firm Prima Materia led a €600 million round into Helsing, the Munich-based defense-AI company that produces the HX-2 strike drone and AI-powered battlefield decision software, taking the company’s valuation to €12 billion [4][45]. Ek chairs the Helsing board.

AI, mass and autonomy are driving the new battlefield.

Daniel Ek, Financial Times interview defending the Helsing investment, June 2025 [45]

The response inside the music community was the inverse of the Rogan controversy. Where Rogan had cost Spotify a handful of legacy folk artists and a media cycle, the Helsing investment caused defections from active mid-career bands across multiple genres. King Gizzard and the Lizard Wizard removed nearly their entire catalog on July 25, 2025 [46]. Massive Attack, the first major-label artist to pull out, described the revenue link from listeners through Spotify to Ek to Helsing’s drones as a moral and ethical burden artists could not carry [47]. Deerhoof, Xiu Xiu, Kalahari Oyster Cult, and dozens of independent labels followed in a slow but visible wave through the second half of 2025 [48].

On September 30, 2025, Ek announced he was stepping down as CEO effective January 1, 2026, and moving to an executive chairman role focused on “the long arc” of Spotify and capital-allocation decisions [2][49]. Gustav Söderström, the company’s longtime CTO and co-president, and Alex Norström, the company’s chief business officer and co-president, became co-CEOs [2].

The first four months of the new regime have produced a striking acceleration. Q1 2026 closed at €4.5 billion of revenue (8% Y/Y reported, 14% on a constant-currency basis), 293 million Premium subscribers (up 9% Y/Y), 761 million monthly users (up 12% Y/Y), and €715 million in operating profit.

Active learning question. You are a Spotify shareholder on May 26, 2026. The company has just printed €715 million of quarterly operating profit and is testing super-premium pricing tiers, fitness, AI music, and a new generative recommender system. Its founder has stepped aside at the moment of maximum momentum and is now devoting his attention to a defense-AI company that is provoking real artist defections. What three metrics in the Q2 2026 print would tell you whether the co-CEO model is working, and what would the failure mode look like?

Lessons

When the structural cost base of your industry consumes 70% of revenue from day one, the only available strategy is to build a second business with different economics on top of the first. Spotify spent its first ten years scaling music, a category in which it could never earn more than about 30% gross margin because of the label royalty floor, and then layered podcasts, audiobooks, and now fitness on top, each with materially better unit economics. The lesson is not that bad-economics businesses should be avoided. It is that they should only be entered if they can act as a moat for a second, better-economics business you intend to build on top.

A free tier is a conversion engine, not a marketing expense, and it only works if the data shows free users are training the recommendation system that paid users will not leave. Spotify’s freemium model is widely copied and almost universally misunderstood. Heavy free listeners do not upgrade in Scandinavia at 20%-plus because the ads got intolerable. They upgrade because by month twelve the personalization on their account is too good to abandon. The free tier produces six to twelve months of listening data per user, which trains a personalization layer that has become switching-cost-grade by the time the user upgrades. Without that loop, freemium is just a cheap-customer-acquisition program with negative gross margin.

A bet that looks like brand suicide is sometimes the cheapest acquisition you will ever do. The Joe Rogan deal was a $200 million transfer to a single creator who, eighteen months later, would generate the largest brand crisis in Spotify’s history. Net of churn, Spotify paid roughly $20 per incremental Rogan-converted Premium subscriber, a customer-acquisition cost that in a market where Spotify’s marketing spend was running at roughly $50 per Premium subscriber was a screaming bargain even after the controversy. The lesson is not that Rogan-style bets are good. It is that the headline cost of a controversial creator deal is usually denominated in brand units, and the brand cost is almost always smaller than the spreadsheet model says it is. The mistake to avoid is the opposite. Declining a high-CAC-displacement deal because the legal and PR teams are louder than the data team usually means leaving incremental scale on the table.

Direct listings, freemium funnels, Discover Weekly, podcast pivots, and three-tier pricing all started as engineering hacks before they became corporate strategy. Discover Weekly was a Hack Week project the engineers built without permission from Ek, who did not initially understand its appeal. The 2018 direct listing was structured by a small group of finance and legal staff against the advice of most of Wall Street. The Echo Nest acquisition was a $100 million bet on a then-obscure MIT spinout. Spotify’s most consequential strategic moves of the past decade were, almost without exception, ideas that lived inside the company at the level of small teams before being absorbed into the corporate plan. The structural lesson for any platform business is that the optimization layer (recommendation, pricing, monetization) is where compounding lives, and the optimization layer cannot be designed top-down. It has to be discovered by people close to the data.

Part II — Financial Deep-Dive

Lens 1: Historical Performance

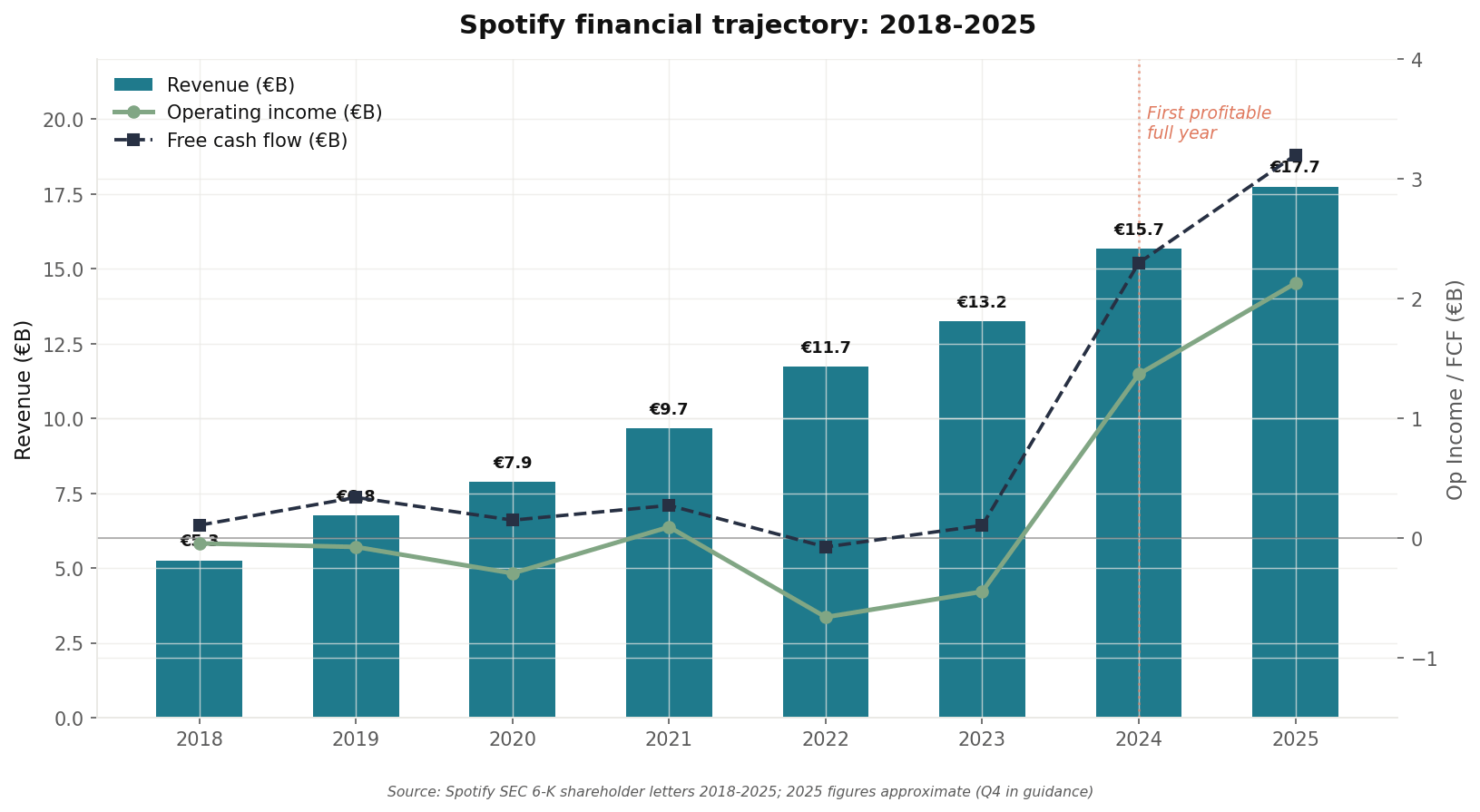

Spotify’s revenue compounded at 18.9% CAGR from 2018’s €5.26B to 2025’s estimated €17.74B [54][55][41]. The shape is not the question. Every audio streamer has grown. The question is the gap between the top line and the bottom line.

For seven of the eight years from 2018 to 2023, Spotify either lost money at the operating line or printed marginal profitability that disappeared the next quarter. The 2020 -€293M operating loss reflected the $200M Joe Rogan deal and the broader €800M+ podcast acquisition push [32][67]. The 2022 -€659M loss reflected the post-pandemic headcount bloat that triggered the 2023 cuts [37]. The breakpoint year is 2024, when operating income inflected to €1.37B (+€1.8B Y/Y swing) and free cash flow tripled to €2.3B [41][55]. Q1 2026 alone printed €715M of operating profit — more than the cumulative operating profit Spotify had produced in the previous 17 years of operation combined [54].

The 2024 inflection has three drivers, in declining order of magnitude:

First, the December 2023 17% layoff (~1,500 jobs) removed €600-700M of run-rate personnel expense from a roughly €4B annual operating expense base [37][38]. The disruption was real — Ek admitted on the Q1 2024 earnings call that operations had been hit harder than expected [40] — but the cost saving showed up immediately. Second, marketplace programs (Discovery Mode, Marquee, Showcase) generated incremental Premium gross margin by selling promotional placement back to labels at a margin take, partially offsetting the underlying royalty cost. Third, the audiobook gross-margin drag (start-up costs through 2023-2024) annualized away by 2025.

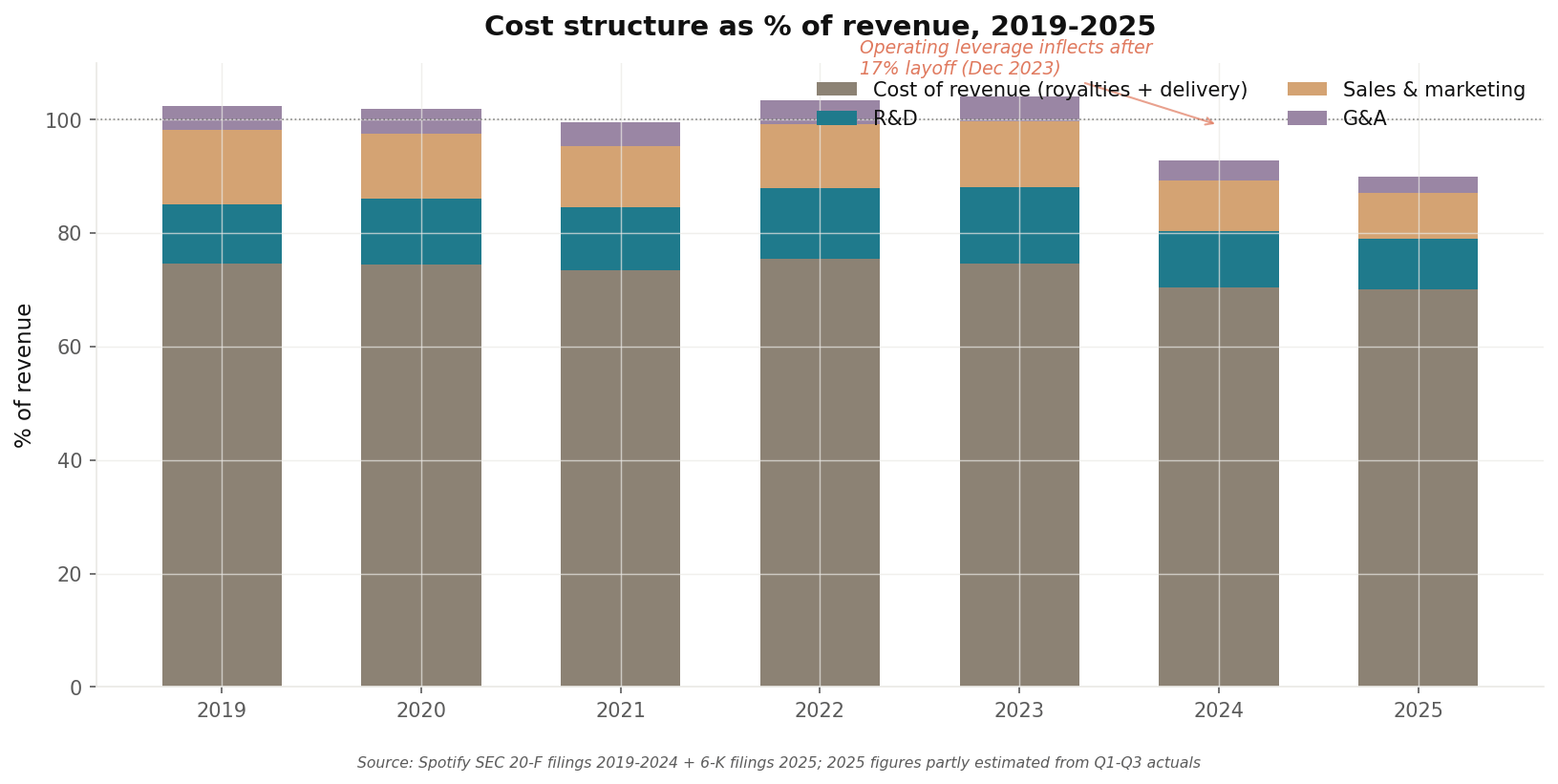

Lens 2: Cost Structure & Operating Leverage

Total cost structure (% of revenue, FY2024):

- Cost of revenue (royalties + delivery): 70.4%

- R&D: 9.9%

- Sales & marketing: 9.0%

- G&A: 3.5%

= Operating margin: 7.3%

Lens 3: Customer Cohort Economics

Each new Spotify subscriber generates roughly €70 of gross profit over their lifetime against approximately €30 of acquisition cost — a healthy 2.3x ratio that does not benefit from the upsell economics typical of B2B SaaS, because Spotify has structurally chosen retention (Family/Duo plans) over revenue expansion (Individual upgrades).

Lens 4: Strategic Optionality

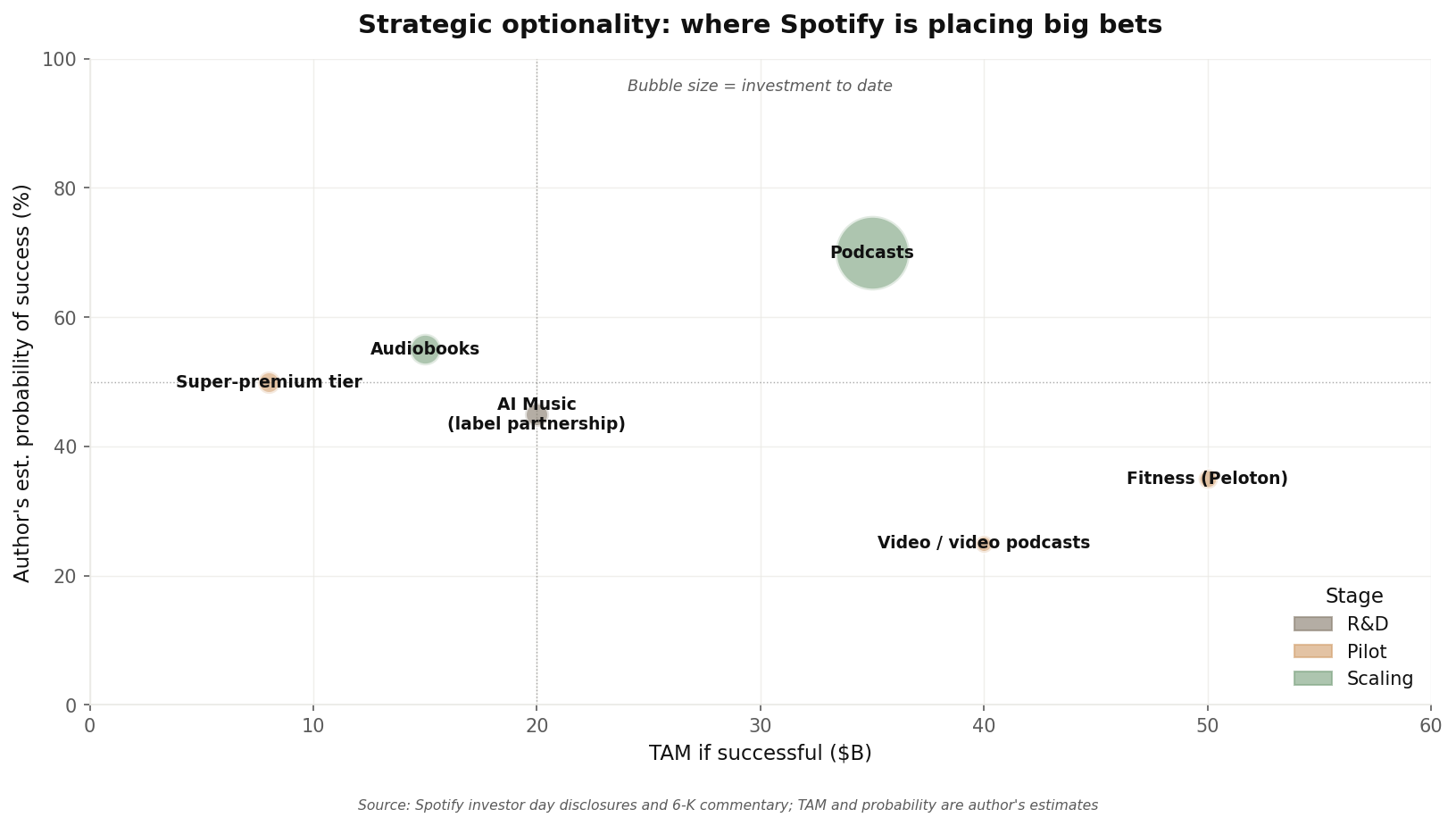

Spotify in 2026 is placing six bets of meaningful size. In order of capital deployed:

Podcasts ($1.3B+ cumulative). Now arguably the only podcast platform that matters at scale: Spotify aggregated more listeners than Apple Podcasts by 2022 [76] and added video podcasting at scale by 2025 [54]. The TAM if podcasts continue to take share from radio is $30-40B globally. Probability of continued dominance: high. This is no longer optionality — it is core business.

Audiobooks ($200M+ cumulative). Audible (Amazon) is the incumbent at roughly $2B in revenue. Spotify entered with the Findaway acquisition (2022), launched the 15-hours-per-month Premium bundle in late 2023, and has expanded to 22+ markets and 700K+ titles by Q1 2026 [54]. The bet is that bundling audiobooks into Spotify Premium is a higher-attach-rate product than charging Audible’s $14.95/month standalone price. Early data is favorable but inconclusive.

Fitness (Peloton, $50M+ committed). Launched April 27, 2026 with 1,400 Peloton classes bundled into Premium [52][53]. The TAM if Spotify becomes the default workout-audio companion is $40-50B globally (against Apple Fitness+, Peloton App, ClassPass, and YouTube workout content). Probability is the lowest of the strategic bets because Spotify is late and has no instructor brand of its own. Watch the Q3 2026 disclosure on fitness category engagement.

AI music ($100M+ in licensing partnerships). The October 2025 deal with UMG, Sony, Warner, Merlin, and Believe — agreeing to AI music product partnerships with proper rights-holders ahead of product launch — is unusual in an industry that has watched OpenAI and Suno launch first and litigate later [50]. The economic mechanism for AI music revenue split is not yet defined.

Super-premium tier ($80M+ in product investment). Lossless audio launched September 2025 — but Spotify deliberately did not gate it behind a higher-priced tier, leaving questions about the super-premium strategy [77]. The three-tier pricing pilot in select emerging markets in late 2025 is the more concrete test. If successful, this is a 10-15% Premium revenue uplift opportunity over 3-5 years.

Video / video podcasts ($30M+ in content investment). 590K+ video podcasts now available [54]. The bet is that video is increasingly how Gen Z consumes long-form audio (per Trevor Noah, Joe Rogan, Lex Fridman shows). Spotify is competing against YouTube’s distribution but with better audio-first economics. Probability moderate; watch retention metrics by content type.

Spotify’s optionality portfolio is well-diversified across mature (podcasts), scaling (audiobooks), and pilot-stage (fitness, AI music, super-premium) bets. Total option value, weighted by probability, is roughly $15-25B of incremental EV — material against the current ~$127B enterprise value but not the kind of single-bet asymmetric upside that Netflix had with originals in 2013 or Amazon had with AWS in 2010.

Citations

[1] Spotify Technology S.A., Form 6-K, Q1 2026 Shareholder Letter, April 2026. https://www.sec.gov/Archives/edgar/data/0001639920/000114036126017211/ef20071303_ex99-1.htm

[2] CNBC, “Spotify founder Daniel Ek stepping down as CEO, company names co-CEOs to replace him,” September 30, 2025. https://www.cnbc.com/2025/09/30/spotify-founder-daniel-ek-stepping-down.html

[3] Spotify Newsroom, “Spotify: A Visual History,” April 2026. https://newsroom.spotify.com/spotify-timeline/

[4] The FADER, “Spotify’s Daniel Ek secures €600 million investment in A.I military drone company,” June 23, 2025. https://www.thefader.com/2025/06/20/spotify-daniel-ek-helsing-investment

[5] Ben Gilbert, LinkedIn note on the Acquired interview with Daniel Ek, May 2023. https://www.linkedin.com/posts/benjamingilbert_spotify-ceo-daniel-ek-acquired-podcast-activity-7064941973761110016-nlK5

[6] Sven Carlsson and Jonas Leijonhufvud, The Spotify Play: How CEO and Founder Daniel Ek Beat Apple, Google, and Amazon in the Race for Audio Dominance, 2021. https://www.everand.com/book/636449456/The-Spotify-Play

[7] CoffeeSpace Blogs, “Spotify Founders’ Journey - The Titan of Music Streaming,” December 2024. https://www.coffeespace.com/blog-post/spotify-founders-journey

[8] Wikipedia, “Daniel Ek,” accessed May 2026. https://en.wikipedia.org/wiki/Daniel_Ek

[9] CNBC, “Spotify CEO Daniel Ek is a billionaire after IPO,” April 2018. https://www.cnbc.com/2018/04/04/spotify-ceo-daniel-ek-is-a-billionaire-after-ipo.html

[10] Marketing4ecommerce, “What is the story behind Daniel Ek, the creator of Spotify,” October 2025. https://marketing4ecommerce.net/en/story-of-the-creator-of-spotify-daniel-ek/

[11] Currency Fund Group, “The story of Daniel Ek - Mr Spotify,” January 2015. http://www.currencyfundgroup.com/2015/01/05/the-story-of-daniel-ek-mr-spotify/

[12] Frederick AI, “Founder Story: Daniel Ek of Spotify,” February 2025. https://www.frederick.ai/blog/founder-story-daniel-ek-of-spotify

[13] Music Business Worldwide, “Daniel Ek, Spotify,” January 2026. https://www.musicbusinessworldwide.com/people/daniel-ek/

[14] businessmodelcanvastemplate.com, “What is Brief History of Spotify Company?,” March 2026. https://businessmodelcanvastemplate.com/blogs/brief-history/spotify-brief-history

[15] Ari’s Take, “Spotify And UMG Rigged The Game a Long Time Ago,” January 2025. https://aristake.com/spotify-and-umg/

[16] whattodoaboutspotify.com, “The Record Label Oligopoly,” August 2025. https://www.whattodoaboutspotify.com/essays/spotify-streaming-rigged-for-major-labels

[17] Acquired podcast, “Spotify CEO Daniel Ek: The Complete History and Strategy,” May 2023. https://www.acquired.fm/episodes/spotify-ceo-daniel-ek

[18] AmpVortex, “Spotify: From a Swedish Anti-Piracy Startup to a Global Audio Empire,” January 2026. https://www.ampvortex.com/spotify-from-a-swedish-anti-piracy-startup-to-a-global-audio-empire/

[19] Alexander Jarvis, “Sean Parker’s Email to Spotify’s Daniel Ek,” February 2025. https://www.alexanderjarvis.com/sean-parker-s-email-to-spotifys-daniel-ek/

[20] The Next Web, “Sean Parker email, pitching Spotify interest in 2009,” October 2011. https://thenextweb.com/news/you-have-to-see-this-email-from-sean-parker-in-2009-pitching-his-interest-in-spotify

[21] The Screenlight, “Spotify: How infamous investor Sean Parker helped the Swedish platform to reach global userbase,” February 2026. https://www.thescreenlight.com/post/spotify-how-infamous-investor-sean-parker-helped-the-swedish-platform-to-reach-global-userbase

[22] Spotify Newsroom, “Spotify: A Visual History” (U.S. launch entry), April 2026. https://newsroom.spotify.com/spotify-timeline/

[23] PortersFiveForce.com, “What is Brief History of Spotify Technology Company?,” January 2026. https://portersfiveforce.com/blogs/brief-history/spotify

[24] Quartz, “The magic that makes Spotify’s Discover Weekly playlists so damn good,” July 2022. https://qz.com/571007/the-magic-that-makes-spotifys-discover-weekly-playlists-so-damn-good

[25] Spotify Engineering blog, “What made Discover Weekly one of our most successful feature launches to date?,” November 2015. https://engineering.atspotify.com/2015/11/what-made-discover-weekly-one-of-our-most-successful-feature-launches-to-date

[26] IEEE Spectrum, “The Little Hack That Could: The Story of Spotify’s Discover Weekly Recommendation Engine,” 2017. https://spectrum.ieee.org/amp/the-little-hack-that-could-the-story-of-spotifys-discover-weekly-recommendation-engine-2650274671

[27] Stratoflow, “Spotify Recommendation Algorithm: What’s The Secret to Its Success?,” May 2025. https://stratoflow.com/spotify-recommendation-algorithm/

[28] TechCrunch, “Spotify founder Daniel Ek admits he initially didn’t get the appeal of the flagship feature Discover Weekly,” September 2023. https://techcrunch.com/2023/09/05/spotify-founder-daniel-ek-admits-he-initially-didnt-get-the-appeal-of-the-flagship-feature-discover-weekly

[29] University of Chicago Law Review, “The Underlying Underwriter: An Analysis of the Spotify Direct Listing,” 2019. https://lawreview.uchicago.edu/print-archive/underlying-underwriter-analysis-spotify-direct-listing

[30] Spotify Technology S.A., SEC Form 424B3, April 2018. https://www.sec.gov/Archives/edgar/data/0001639920/000119312518149451/d579509d424b3.htm

[31] CNBC, “Full transcript: Spotify CEO Daniel Ek discusses podcasts and competing with tech giants,” February 2019. https://www.cnbc.com/2019/02/06/full-transcript-spotify-ceo-daniel-ek-on-cnbc.html

[32] NME / New York Times reporting, “Spotify said to have paid $200million for Joe Rogan podcast deal, twice the figure previously reported,” February 2022. https://www.nme.com/news/music/spotify-said-to-have-paid-200million-for-joe-rogan-podcast-deal-twice-the-figure-previously-reported-3164283

[33] Inverse, “Spotify’s deal with Joe Rogan is worth $200 million, actually,” February 2022. https://www.inverse.com/input/culture/spotify-deal-joe-rogan-worth-200-million-covid-misinformation

[34] Fox Business, “Spotify’s deal with Joe Rogan is reportedly worth ‘at least’ $200 million,” February 2022. https://www.foxbusiness.com/entertainment/spotify-joe-rogan-deal-200-million-deal-report

[35] Fox News, “Joe Rogan says he gained ‘2 million subscribers’ during cancel culture campaign,” 2022. https://www.foxnews.com/media/joe-rogan-gained-2-million-subscribers-spotify.amp

[36] Sportskeeda, “Why did Apple remove the Joe Rogan Experience? Exploring the UFC commentator’s podcast platform over three years,” 2024. https://www.sportskeeda.com/mma/news-why-apple-remove-joe-rogan-experience-exploring-ufc-commentator-s-podcast-platform-three-years

[37] Fortune, “Spotify layoffs: CEO Daniel Ek cuts 17% of bloated workforce,” December 4, 2023. https://fortune.com/europe/2023/12/04/daniel-ek-to-slash-bloated-spotify-headcount-by-17-after-blasting-staff-for-doing-work-around-the-work/

[38] CNBC, “Spotify jumps after saying it will cut 17% of workforce — read the full memo from CEO Daniel Ek,” December 4, 2023. https://www.cnbc.com/2023/12/04/spotify-to-lay-off-17percent-of-employees-ceo-daniel-ek-says.html

[39] Fast Company, “Spotify ends 2023 with more mass layoffs as CEO Daniel Ek announces 3rd round of job cuts,” December 2023. https://www.fastcompany.com/90992072/spotify-mass-layoffs-december-2023-3rd-round

[40] TheStreet, “Spotify CEO is shocked by negative impact of recent layoffs,” April 2024. https://www.thestreet.com/employment/spotify-ceo-is-shocked-by-negative-impact-of-recent-layoffs

[41] Yahoo Finance / Variety, “Spotify Posts First Full-Year Profit for 2024, CEO Says Streamer Will ‘Double Down’ on Music in 2025,” February 2025. https://finance.yahoo.com/news/spotify-posts-first-full-profit-145317904.html

[42] ProMarket / University of Chicago, “The European Commission Fines Apple 1.84 Billion Euros and Spotify Still Isn’t Happy,” March 19, 2024. https://www.promarket.org/2024/03/19/the-european-commission-fines-apple-1-84-billion-euros-and-spotify-still-isnt-happy/

[43] Fortune, “Spotify CEO Daniel Ek takes aim at Apple in video message following $1.84 billion court victory,” March 5, 2024. https://fortune.com/2024/03/05/apple-spotify-daniel-ek-european-commission-antitrust

[44] Quantfury, “Spotify’s bet on audiobooks and podcasts has been successful,” October 2025. https://quantfury.com/market-insights/spot-2/

[45] Truthbit AI / Medium summary of FT reporting, “Who Invests $700M in Military Drones? The Man Who Streams Your Music,” October 2025. https://medium.com/@truthbit.ai/who-invests-700m-in-military-drones-the-man-who-streams-your-music-93a16e7a395a

[46] DroneXL, “Bands Boycott Spotify Over CEO’s Investment In Drones,” August 2025. https://dronexl.co/2025/08/04/bands-boycott-spotify-ceo-helsing-drones/

[47] EBU Spotlight, “Behind the Spotify boycott: Daniel Ek, military AI, and the misinformation linking Helsing to Israel,” November 2025. https://spotlight.ebu.ch/p/behind-the-spotify-boycott-daniel

[48] Euronews, “We don’t want our music killing people: artists revolt against Spotify over AI warfare ties,” July 2025. https://euronews.com/culture/2025/07/30/we-dont-want-our-music-killing-people-artists-revolt-against-spotify-over-ai-warfare-ties

[49] Music Business Worldwide, “Daniel Ek steps away from CEO role at Spotify to become Executive Chairman; Gustav Söderström and Alex Norström named co-CEOs,” September 30, 2025. https://www.musicbusinessworldwide.com/daniel-ek-to-step-away-from-ceo-role-at-spotify-will-become-executive-chairman-effective-january-1-2026/

[50] The Hollywood Reporter, “Spotify to Develop AI Music Products in Partnership With Major Record Labels,” October 16, 2025. https://www.hollywoodreporter.com/music/music-industry-news/spotify-ai-music-partnership-with-record-labels-1236402698/

[51] Music Business Worldwide, “Spotify plans to hike US subscription prices in Q1 2026 (report),” November 2025. https://www.musicbusinessworldwide.com/spotify-plans-us-price-hike-in-q1-2026-report/

[52] Variety, “Spotify Muscles Into Fitness Category, Inks Deal With Peloton for 1,400-Plus Workout Videos,” April 27, 2026. https://variety.com/2026/digital/news/spotify-fitness-peloton-guided-workout-videos-1236727258/

[53] Axios, “Spotify adds Peloton workouts in fitness expansion,” April 27, 2026. https://www.axios.com/2026/04/27/spotify-premium-peloton-fitness

[54] Spotify Technology S.A., Form 6-K, Q1 2026 Shareholder Letter, April 2026. (Same as case study [1].) https://www.sec.gov/Archives/edgar/data/0001639920/000114036126017211/ef20071303_ex99-1.htm

[55] Spotify Technology S.A., Form 20-F FY2024, February 2025. https://www.sec.gov/Archives/edgar/data/0001639920/000163992025000003/spot-20241231xexx21.htm

[56] Spotify Technology S.A., Form 6-K Q4 2020 Shareholder Letter, February 2021. https://www.sec.gov/Archives/edgar/data/0001639920/000119312521026331/d63624dex991.htm

[57] Spotify Technology S.A., Form 6-K Q4 2021 Shareholder Letter, February 2022. https://www.sec.gov/Archives/edgar/data/0001639920/000114036122003619/brhc10033384_ex99-1.htm

[58] Music Business Worldwide, “Spotify subscriber base grew by 3m to 293m in Q1,” April 2026. https://www.musicbusinessworldwide.com/spotify-subscriber-base-grew-by-3m-to-293m-in-q1-company-posted-837m-operating-profit-for-the-quarter/

[59] Spotify Technology S.A., Form 6-K Q1 2025 Shareholder Letter (buyback program disclosure), April 2025. https://www.sec.gov/Archives/edgar/data/0001639920/000163992025000006/spot-20250331x6xk.htm

[60] Billboard, “Spotify Announces Another Stock Buyback of Up to $1 Billion,” August 20, 2021. https://www.billboard.com/pro/spotify-stock-price-buyback-1-billion/

[61] Stocktitan / Spotify Q1 2026 financial summary, April 2026. https://www.stocktitan.net/sec-filings/SPOT/6-k-spotify-technology-s-a-current-report-foreign-issuer-a1761adf2124.html

[62] Music Business Worldwide, Q1 2026 regional breakdown. https://www.musicbusinessworldwide.com/spotify-subscriber-base-grew-by-3m-to-293m-in-q1-company-posted-837m-operating-profit-for-the-quarter/

[63] Variety, “Spotify Q1 Revenue Rises 8%, Premium Subscribers Inch Up to 293 Million Amid U.S. Price Hikes,” April 2026. https://variety.com/2026/music/news/spotify-q1-2026-earnings-revenue-total-premium-subscribers-1236731842/

[64] Music Week, “Spotify Loud & Clear 2025 report breaks down its $10 billion role in the streaming economy,” March 2025. https://www.musicweek.com/digital/read/spotify-loud-clear-2025-report-breaks-down-its-10-billion-role-in-the-streaming-economy/091558

[65] Spotify Newsroom, “As Spotify Turns 20, the Most Global and Diverse Music Industry in History Has Taken Shape — Loud & Clear 2025,” March 11, 2026. https://newsroom.spotify.com/2026-03-11/loud-and-clear-music-economics-highlights/

[66] Spotify Technology S.A., Form 6-K Q1 2025 Cash Flow Statement (SBC disclosure), April 2025. https://www.sec.gov/Archives/edgar/data/0001639920/000114036125016186/ef20047937_ex99-1.htm

[67] Spotify Technology S.A., Form 6-K Q1 2021 Shareholder Letter (churn commentary), April 2021. https://www.sec.gov/Archives/edgar/data/0001639920/000119312521135262/d162701dex991.htm

[68] Spotify Technology S.A., Form 6-K Q3 2020 Shareholder Letter (churn falls below 4%), October 2020. https://www.sec.gov/Archives/edgar/data/0001639920/000119312520280367/d92783dex991.htm

[69] June.so, “Spotify Metrics: Reverse Engineering Retention Rate & Churn,” September 2024. https://www.june.so/blog/reverse-engineering-spotifys-saas-metrics

[70] Digital Music News, “US Music Streaming Market Shares Are Holding Steady in 2025,” August 2025. https://www.digitalmusicnews.com/2025/08/21/music-streaming-market-share-data-august-2025/

[71] Spliiit blog, “Music Streaming in 2026: A Comparison of Spotify, Apple Music, Deezer, and YouTube Music,” April 2026. https://www.spliiit.com/en/blog/streaming-musique-comparatif-2026

[72] Digital Music News, “YouTube Music Struggles Against Spotify, Apple, and Amazon,” October 2025. https://www.digitalmusicnews.com/2025/10/23/youtube-music-struggle-against-spotify-apple-music-amazon-music/

[73] Variety, “Spotify Buys Podcast Ad-Tech Firm Megaphone for $235 Million in Cash,” November 2020. https://variety.com/2020/digital/news/spotify-buys-megaphone-podcast-advertising-1234826863/

[74] Music Business Worldwide, “Spotify has spent $1.2bn+ on companies to scale its non-music business over the past 3 years,” August 2022. https://www.musicbusinessworldwide.com/spotify-has-spent-1-2bn-on-companies-to-scale-its-non-music-business-over-the-past-3-years/

[75] Architeg Prints, “Spotify Faces ‘Payola’ Lawsuit Over Discovery Mode,” November 2025. https://www.architeg-prints.com/blog/spotify-faces-payola-lawsuit-over-discovery-mode-what-you-need-to-know

[76] Acquired podcast / Acquired Briefing summary of Spotify-podcasting market share, May 2023. https://www.acquired.fm/episodes/spotify-ceo-daniel-ek

[77] Music Business Worldwide, “Spotify plans to hike US subscription prices in Q1 2026 (report)” (lossless feature commentary), November 2025. https://www.musicbusinessworldwide.com/spotify-plans-us-price-hike-in-q1-2026-report/

[78] Ari’s Take, “Spotify And UMG Rigged The Game a Long Time Ago,” January 2025. (Same as case study [15].) https://aristake.com/spotify-and-umg/

[79] Billboard, “Spotify Lawsuit Says ‘Discovery Mode’ Is Just ‘Modern Payola’,” November 5, 2025. https://www.billboard.com/pro/spotify-lawsuit-discovery-mode-modern-payola/