BCW 35: Unitree

A case study about World’s Best-Selling Humanoid Robot

Welcome to the 36 of you who joined Business Case Weekly this week

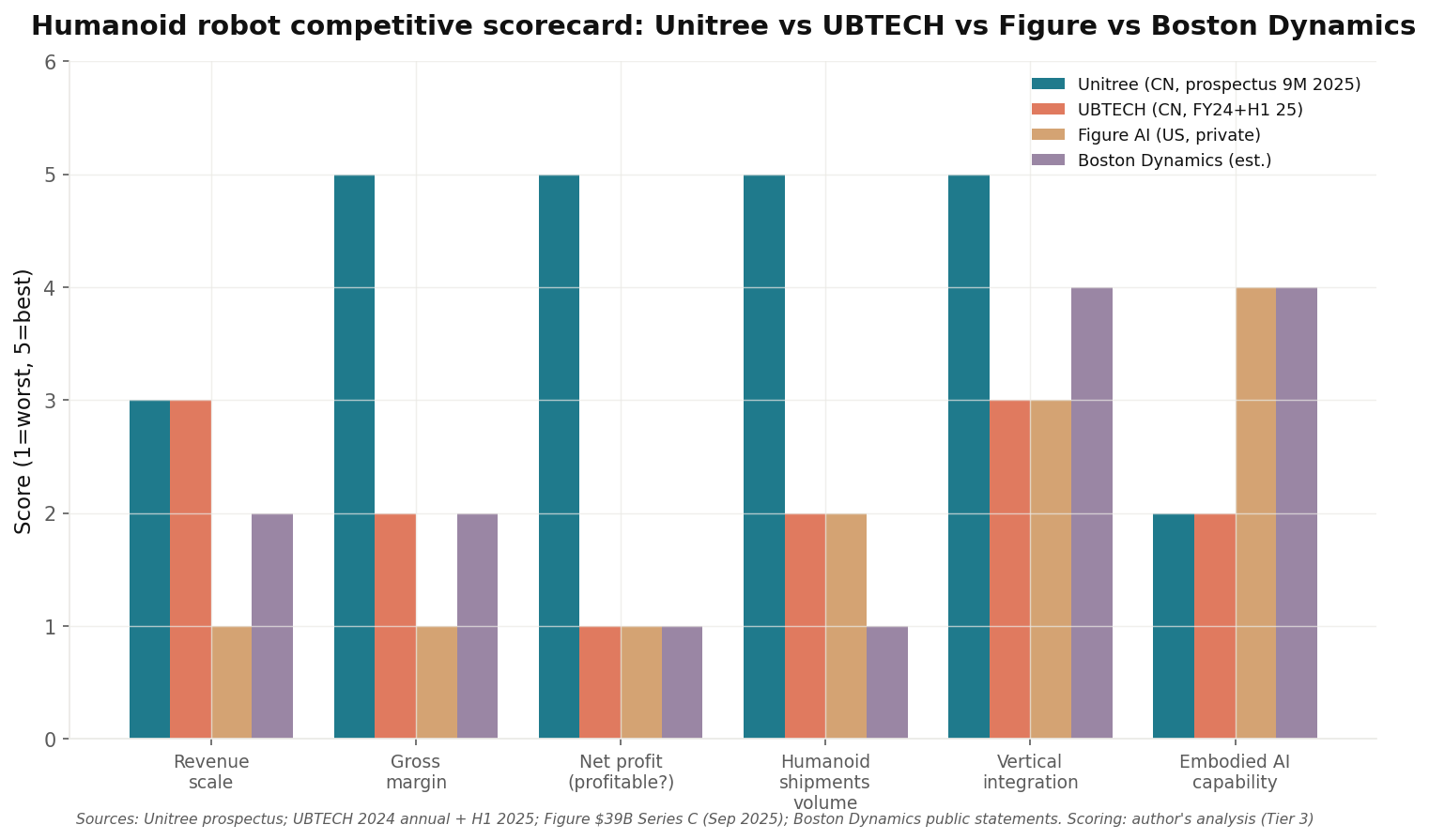

Unitree Robotics is the only profitable humanoid robot company at meaningful scale.

In 2025 it shipped 5,500-plus humanoid units, took 32.4% of global humanoid shipments, recorded ¥1.71 billion ($250 million) in revenue, and posted ¥600 million in adjusted net profit [13][14][15], all while Boston Dynamics, Figure, and Tesla still burned cash.

The company did this not by inventing better robots than the West, but by treating cost as the only KPI for nine years [35] and selling research-grade hardware to academia for a tenth of the price of any competitor.

The story is unusual because the founder, Wang Xingxing, is a Chinese engineer who flunked English exams, missed admission to Zhejiang University, and built his first prototype on a ¥20,000 ($3000) budget for a master’s thesis [3].

The question now in front of a probable $7 billion IPO valuation [38] is whether the discipline that won the hardware race can win the AI race that follows.

Two Months at DJI, 2009–2017

In June 2016, Wang Xingxing defended his master’s thesis at Shanghai University. The committee watched a video of XDog, a small four-legged robot that he had built over the previous year, walking forward, backward, and sideways using brushless DC motors of his own design [4][5].

Within days the video was circulating on Chinese tech media, then on robotics blogs in the United States and Germany.

Wang had already accepted a job at DJI, the Shenzhen drone maker founded by Frank Wang Tao. He moved south, started his probation period, and waited. Within two months the messages arrived: investors offering money, customers offering to buy.

He had to choose between a probationary engineer’s salary at China’s most successful hardware company and an offer of ¥2 million in angel funding to build something that did not yet exist as a category. He chose to resign. On August 26, 2016, he registered Hangzhou Yushu Technology Co., Ltd. (doing business as Unitree) in a 50-square-meter office in Binjiang District [4][5][20].

Born in 1990 in Yuyao, Zhejiang, the son of an ordinary family, Wang had been considered a “slow child” by his teachers and a poor performer at English. His English scores dragged his university admission down.

He missed Zhejiang University and ended up at Zhejiang Sci-Tech University, a tier below, majoring in mechatronics engineering [3][7]. What he had instead was hands. As a first-year undergraduate he built a small bipedal walking robot from scavenged parts.

Without equipment, I used a small hand drill, file, and scissors; without funds, I bought parts for 9 RMB and scavenged unwanted scrap materials. In the end, with just 200 RMB, I made a small bipedal robot.

200 RMB - $30 US Dollars. Wang Xingxing, interview with Chinese media via Our China Story, 2025 [3]

The most prominent platforms then were the BigDog and Spot from Marc Raibert’s Boston Dynamics, the MIT spin-out then owned by Google. Hydraulic actuation gave high force but required heavy pumps, expensive valves, and noisy operation; Wang’s bet was that brushless DC motors with custom controllers could deliver “good enough” performance at a fraction of the cost.

Asked early on whether he planned to compete with Boston Dynamics by selling abroad, he said:

I won’t have this difficulty because my English is poor, and it might be challenging for me to go abroad, so this situation won’t happen, and I don’t need to consider this issue.

Wang Xingxing, early interview with Chinese tech publication, c. 2017–2018, cited in AIProem [20]

The remark looked self-deprecating. It was also strategy by accident.

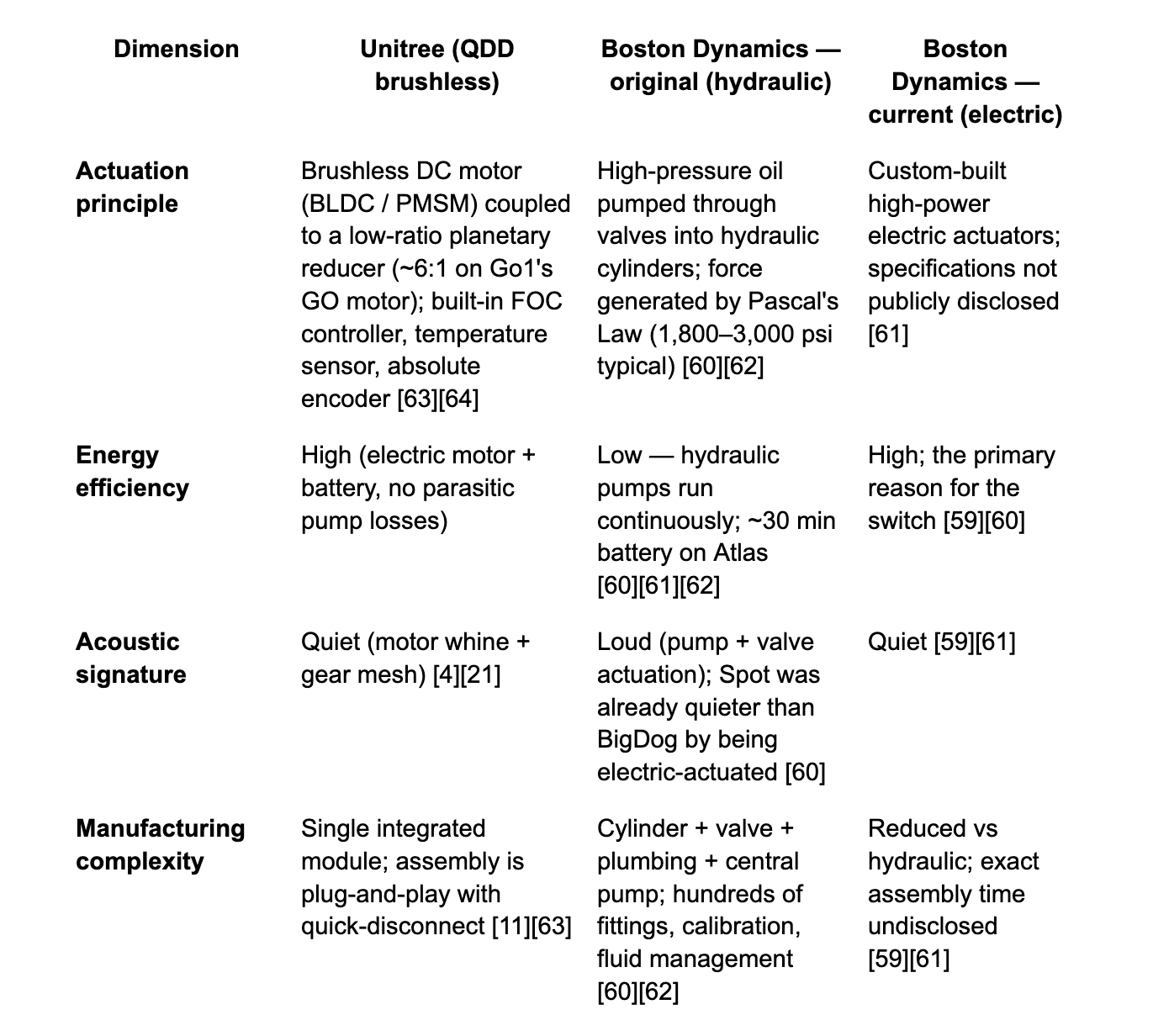

Unitree vs Boston Dynamics comparison

The single most consequential engineering decision separating the two companies is how they convert stored energy into motion. Boston Dynamics’ founding-era robots (BigDog 2005, Atlas 2013, the original Spot 2015) were built around hydraulic actuators because nothing else could deliver the force-density needed for parkour-grade dynamics [59][60][62].

Unitree was founded in 2016 with the opposite bet: that brushless DC motors in a quasi-direct-drive (QDD) configuration could deliver “good enough” performance at a fraction of the cost, weight, and serviceability burden of hydraulics [4][20][21]. The decision compounded for a decade. By April 2024 Boston Dynamics retired hydraulic Atlas in favor of an all-electric replacement [59][61] — implicit acknowledgment that Unitree’s thesis had won at the architecture level. The remaining gap, summarized below, is now about implementation maturity rather than approach.

Bargain with Academia, 2017–2022

The first product, Laikago, launched in 2017 and was named after Laika, the Soviet space dog who orbited Earth in Sputnik 2 in 1957.

Pre-orders opened that year; first shipments went out in 2018 [1][6]. The early customer base was almost entirely universities and research labs. Unitree had a problem and a calling-card both wrapped into one. Wang has been blunt in interviews about why this customer base mattered.

Customers’ willingness to pay for your products is the real commercial closed-loop. Otherwise, it’s always a failed product.

Wang Xingxing, interview with GeekPark, cited in 36Kr, 2025 [35]

The path-not-taken in this period was the Boston Dynamics path. Take government and military money, build the most capable robot in the world at $74,000 per unit, hand-pick a handful of corporate research customers, and pursue commercialization as a slow side-quest. Boston Dynamics began retailing Spot in 2020 at roughly $74,000 [21]. The steelman ran like this. Government contracts paid R&D bills, locked in defense relationships, and avoided the messy work of selling to thousands of underfunded academic labs. A well-funded competitor in 2017 would have copied Boston Dynamics, not undercut them.

Unitree did the opposite. Wang targeted research institutions as the core target users, priced for them, and used the resulting cash flow to fund the next round of R&D. The result was a tight loop of academic sales paying for component development paying for the next product.

The deeper bet underneath the pricing was vertical integration. From the start Wang built motors, reducers, encoders, and controllers in-house. When asked why, he answered with logistics rather than ideology. In the 2017–2018 supply environment, custom components carried high procurement costs and long communication and time costs from suppliers. Building a motor was cheaper than ordering one. The compounding effect of that decision was massive. Six years later, the same custom motor architecture would translate directly into humanoid joints.

Wang told IEEE Spectrum about the 2021 Go1 that the product was the result of six to seven years of hardware iteration aimed at simultaneously achieving ultra-low cost, high reliability, and high performance, and that Unitree had spent more time and money on mechanical hardware than on software [21].

Cost has always been our KPI for everything. The core is to make money.

Wang Xingxing, interview cited in 36Kr, 2025 [35]

The numbers tell the discipline. Unitree launched the Go1 quadruped at $2,700, roughly one-twentieth the price of a Spot [21]. By 2020 the company was profitable, and it stayed profitable every subsequent year [6].

The vertical-integration bet held. Sequoia China, Shunwei Capital, Vertex Ventures, and Matrix Partners came in across A and B rounds in 2020–2022. Meituan joined at the B+ round in 2022 and would eventually become Unitree’s second-largest shareholder behind Wang at roughly 8.24% [9][39].

By 2023 Unitree controlled an estimated 69.75% of global quadruped shipments and 40.65% of dollar market share [6][20]. The company had become, in industry slang, the “price butcher,” a label Wang accepted publicly. Asked in August 2024 whether he could go even lower, he was direct.

I can make the price even lower, but I don’t want to.

Wang Xingxing, interview, August 2024, cited in 36Kr [35]

The marketing was deliberate but cheap. In February 2021, twenty-four Go1 quadrupeds disguised as oxen danced with Andy Lau, the Hong Kong superstar, on the CCTV Spring Festival Gala [4][6]. The Gala is the most-watched single broadcast on earth, with audience reach in the billions. In 2022, 109 Go1 units performed at the Beijing Winter Olympics opening ceremony [4]. Each appearance was free television to engineering departments worldwide. By the time Western media discovered Unitree, every serious robotics PhD program already had at least one Go in the lab.

Active learning questions. You are an investor in 2018. Unitree is selling research-grade quadrupeds to Chinese universities at one-fifth Boston Dynamics’ price, has no military contracts, and the founder cannot give a presentation in English. Do you write a check at the price they are asking? What revenue-per-unit and unit-volume thresholds would change your mind?

The Humanoid Bet, 2023–2025

In 2022, Tesla released Optimus prototypes. In 2023, ChatGPT made foundation models the default lens through which every venture investor evaluated robotics. The category that Boston Dynamics had been quietly working on for two decades, and that Honda had quietly worked on for three, suddenly looked imminent. Wang had been resistant to humanoid investments before. He had believed the technology was not yet ready for implementation. In 2023 he changed his mind.

Humanoids were a different mechanical problem (bipedal balance is harder), a different software problem (manipulation matters more than locomotion), and a market that did not yet have a single proven commercial use case.

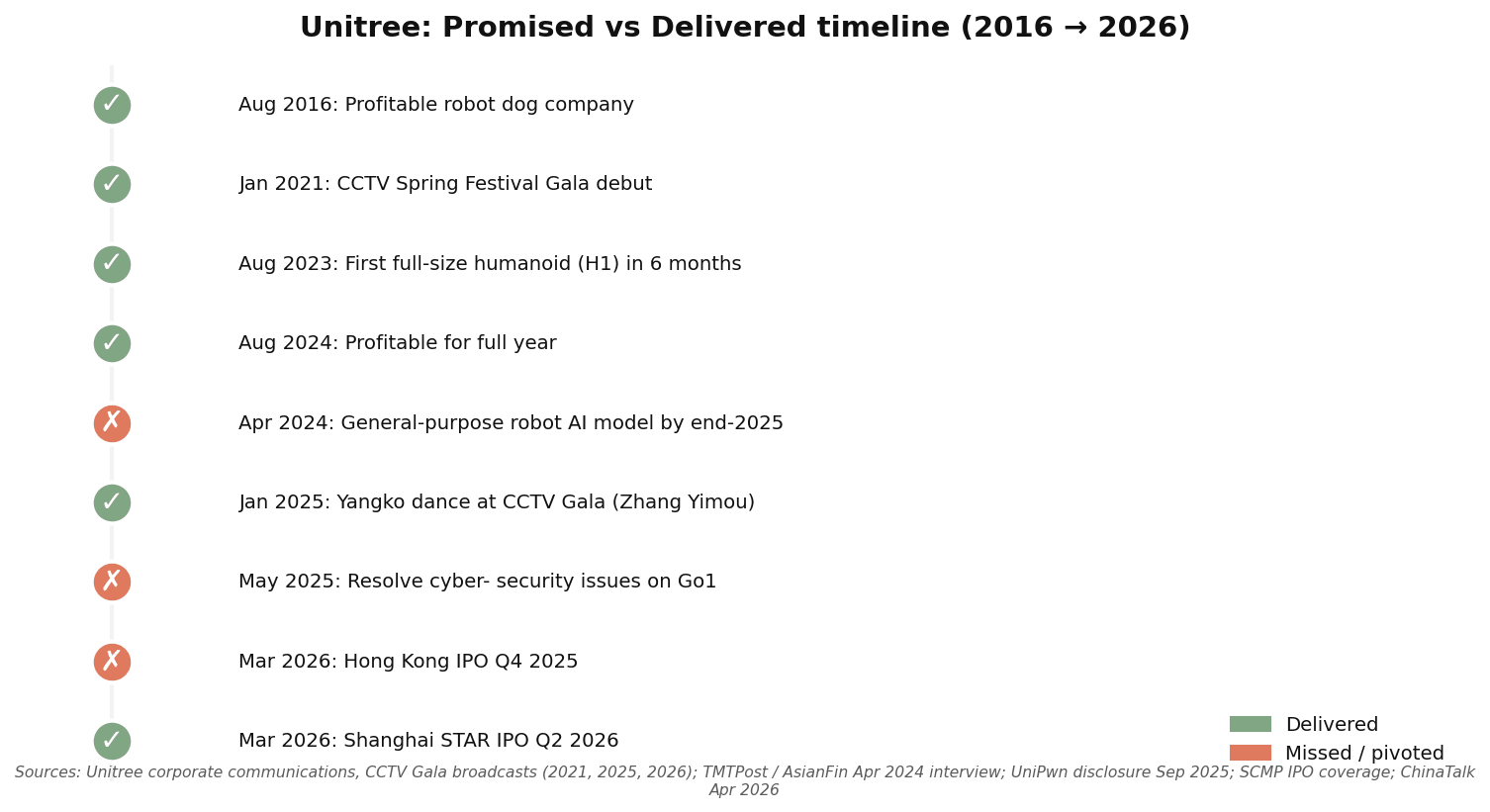

In 2023 he formally established the humanoid project. Six months later, in August 2023, Unitree shipped the H1, described publicly as China’s first full-sized general-purpose humanoid robot capable of running [22]. The H1 set a world running record for an electric biped at 3.3 m/s and, by early 2024, became the first full-sized electric humanoid to complete a standing backflip [22]. Unitree completed first commercial deliveries of H1 in October 2023 at around ¥650,000 (roughly $90,000) per unit, perhaps a third of the cost of any comparable Western full-sized humanoid then in existence [6][22].

The reason the H1 could ship six months from project kickoff was the previous decade of quadruped components. Wang explained at the Snowball Carnival that quadruped robot dogs and humanoid robots share many designs, including joint motors, overall mechanical structure, and sensors [18]. The motors that drove a Go1’s hip drove an H1’s. The control loops translated. The supply chain was the same supply chain. Six years of cost discipline on quadrupeds had built the cheapest humanoid joint motor in the world without anyone noticing.

Boston Dynamics has been working on robots for many years and has also been pursuing commercialization for a long time. The only surprising thing is that back in 2018, I assumed Boston Dynamics had already started developing an electric-driven version. But later, I realized they hadn’t made much progress, and I eventually forgot about it.

Wang Xingxing, interview with TMTPost / AsianFin, April 2024 [18]

In May 2024, at ICRA, Unitree introduced the G1, a smaller humanoid at 127 centimeters and 35 kilograms, with 23 to 43 degrees of freedom depending on configuration, priced at $16,000 [1][6].

The price compressed the humanoid category from “moonshot” to “research budget item.” A later mass-production G1 update brought the entry price to ¥99,000 (about $13,560), described in Chinese coverage as one of the most affordable serious humanoids on the market [6].

Then came the moment that broke Unitree out of robotics-trade-press obscurity into household territory in China.

On the evening of January 28, 2025, sixteen Unitree H1 humanoids took the stage at the CCTV Spring Festival Gala [23][24][25]. Directed by Zhang Yimou, the fifth-generation Chinese filmmaker behind the Beijing 2008 Olympics opening ceremony and the films Hero and Raise the Red Lantern, the act was titled “Yangge Bot.”

Yangko is a vibrant northeastern Chinese folk dance involving rhythmic waist-twisting, leg-kicking, and the spinning of red handkerchiefs [23][25]. The robots, in floral padded jackets, performed the routine alongside human dancers from the Xinjiang Art Institute, executing automated stage position changes driven by AI rather than scripted choreography [23][24]. Total Spring Festival Gala media reach that year was reported by China Media Group at 16.8 billion impressions [24].

Our ultimate goal is to have AI-powered robots take on arduous work for humans, but before that’s achievable, participating in performances allows us to showcase real technological progress and generate some commercial value.

Wang Xingxing, on the strategy behind the Gala appearance, cited by The Robot Report, June 2025 [19]

The performance changed Unitree’s capital terms overnight. In June 2025, Tencent, Alibaba, Ant Group, China Mobile’s fund, Geely Capital, and Jinqiu Capital co-led a Series C round of approximately ¥700 million ($97.6 million), with HongShan Capital also participating, valuing the company at over ¥12 billion (~$1.7 billion) [19][37].

Secondary-market trades of older shares reportedly priced the company above ¥15 billion in the first half of 2025 [36].

Wang himself moved from technical-press subject to political symbol. On February 17, 2025, three weeks after the Gala, the 35-year-old Wang sat in the front row at Xi Jinping’s high-profile private-sector symposium in Beijing. He was the youngest person at the table, alongside Huawei’s Ren Zhengfei, Alibaba’s Jack Ma, BYD’s Wang Chuanfu, Xiaomi’s Lei Jun, and Tencent’s Pony Ma [7][34].

Artificial-intelligence-driven robots are evolving at an incredibly fast pace, surpassing my expectations. Every day brings new surprises. I believe that by the end of the year, humanoid robots will reach a whole new level.

Wang Xingxing, interview with CCTV after the Xi symposium, February 2025 [44]

Active learning questions. You are on Unitree’s small leadership team in early 2023. The quadruped business is profitable, holds roughly 70% global share, and is throwing off cash. You are debating whether to commit roughly 40% of next year’s R&D to humanoids. What evidence would you need before greenlighting it? What would convince you to wait until 2025 instead?

Trojan Horses and Wormable Backdoors, 2024–2025

The humanoid pivot lifted Unitree’s revenue and valuation. It also lifted its threat surface. By mid-2024 Unitree had become a category symbol on two continents, which meant the same robots that danced on Chinese television were also showing up in places that drew the attention of the US national-security apparatus.

In May 2024, The Guardian reported that a Unitree Go2 with an automatic rifle mounted on its back was visible in CCTV footage of Chinese-Cambodian joint military drills.

Unitree responded that it does not sell to the People’s Liberation Army [26][27]. In May 2025, every member of the US House Select Committee on China, Republicans and Democrats together, signed a bipartisan letter requesting the Federal Communications Commission, the Department of Defense, and the Department of Commerce investigate Unitree for alleged ties to the PLA and military-civil fusion programs [26][27].

The fact that PLA-connected robots are operating in U.S. prisons and even within Army operations should be a wake-up call. These machines are not just tools — they are potential surveillance devices backed by the Chinese Communist Party.

Rep. John Moolenaar, Chair of the House Select Committee on the Chinese Communist Party, statement on the bipartisan Unitree letter, May 2025 [26]

The technical case underneath the political letter mattered more than the rhetoric.

In March and April 2025, security researchers Andreas Makris and Kevin Finisterre, independent investigators known for vulnerability disclosures, published findings that Unitree’s Go1 robot dogs shipped with a hidden remote-access tunnel called CloudSail [29][30][31].

CloudSail, built on a third-party Chinese remote-management service from Zhexi Technology, connected each robot silently to a server in China; researchers found roughly 1,900 robots already connected to the tunnel, with no authentication barrier and no disclosure to end users. Anyone with the right API key could stream camera feeds, pull SSH access, and run commands as root [28][29][30].

Unitree’s response was that the issue had been a third-party cloud key compromise that hackers had exploited, not an intentional backdoor, and that the service had been disabled. It also said newer models such as the Go2 and humanoids ran a “more secure upgraded version” and were unaffected [29].

That last claim aged badly. On September 20, 2025, Makris and Finisterre published UniPwn, a critical command-injection vulnerability in the Bluetooth Low Energy (BLE) Wi-Fi configuration interface used by the Go2 and B2 quadrupeds and the G1 and H1 humanoids [28][32].

The exploit allowed root access via a malicious string sent during onboard Wi-Fi setup, then chained into a wormable attack: an infected robot could scan for other Unitree robots in BLE range and compromise them automatically, creating a self-propagating robot botnet [28][32]. The researchers had first contacted Unitree in May; communications stalled in July, and the disclosure went public [28].

We have had some bad experiences communicating with them. So we need to ask ourselves — are they introducing vulnerabilities like this on purpose, or is it sloppy development? Both answers are equally bad.

Andreas Makris, security researcher, interview with IEEE Spectrum, October 2025 [28]

The honest read on this period is that Unitree’s nine-year culture of treating cost as the primary KPI, the same culture that made it the only profitable humanoid company in the world, also produced a security posture roughly consistent with an academic startup, deployed at the scale of critical infrastructure.

The vulnerabilities were not catastrophic in customer impact, but they handed US policy hawks a clean technical case for adding Unitree to the Entity List. As of May 2026 that listing has not happened, but the political ceiling on Unitree’s US commercial expansion is materially lower than it was eighteen months earlier.

Active learning question. You are Unitree’s CEO in May 2025, the day after the bipartisan House Select Committee letter is published. Do you (a) hire a Western-trained CISO and publish a public security roadmap, (b) treat the issue as a geopolitical attack and double down on the China-and-Global-South market, or (c) split the company so that products sold to US institutions run on a separate, audited firmware stack? What does each path cost you in revenue and time?

The IPO and the Brain Problem, 2025–Present

By summer 2025 Unitree was simultaneously the most-watched Chinese hard-tech company outside DeepSeek, the only profitable humanoid company at scale, and the subject of bipartisan US national-security legislation.

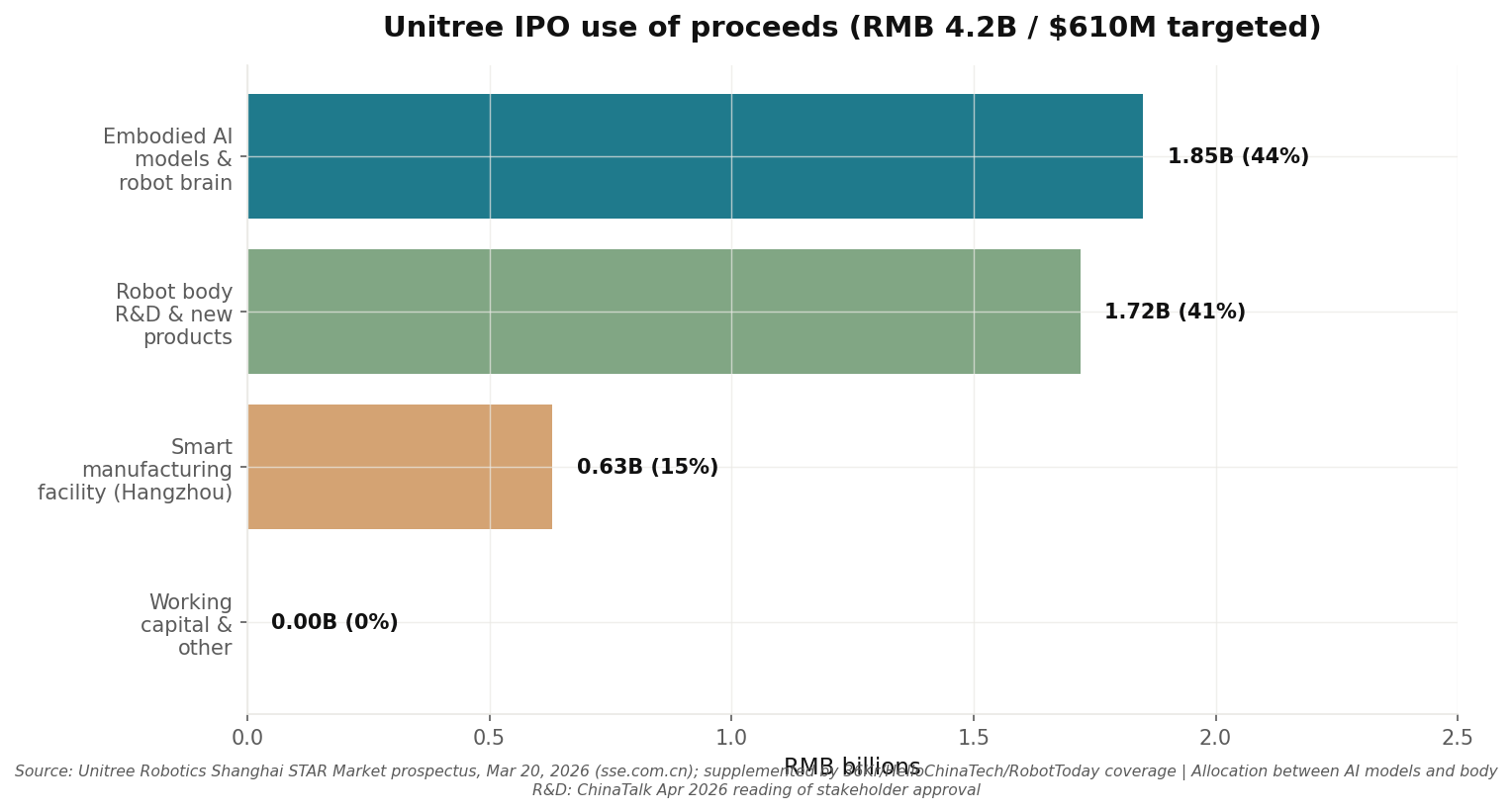

In July 2025, Unitree formally began IPO tutoring with CITIC Securities. The original plan had been a Hong Kong listing. By late 2025, the company had pivoted to the Shanghai Stock Exchange’s STAR Market, a tech-focused board launched in 2019 to anchor strategic Chinese hard-tech listings on the mainland, at a target valuation around $7 billion [9][38].

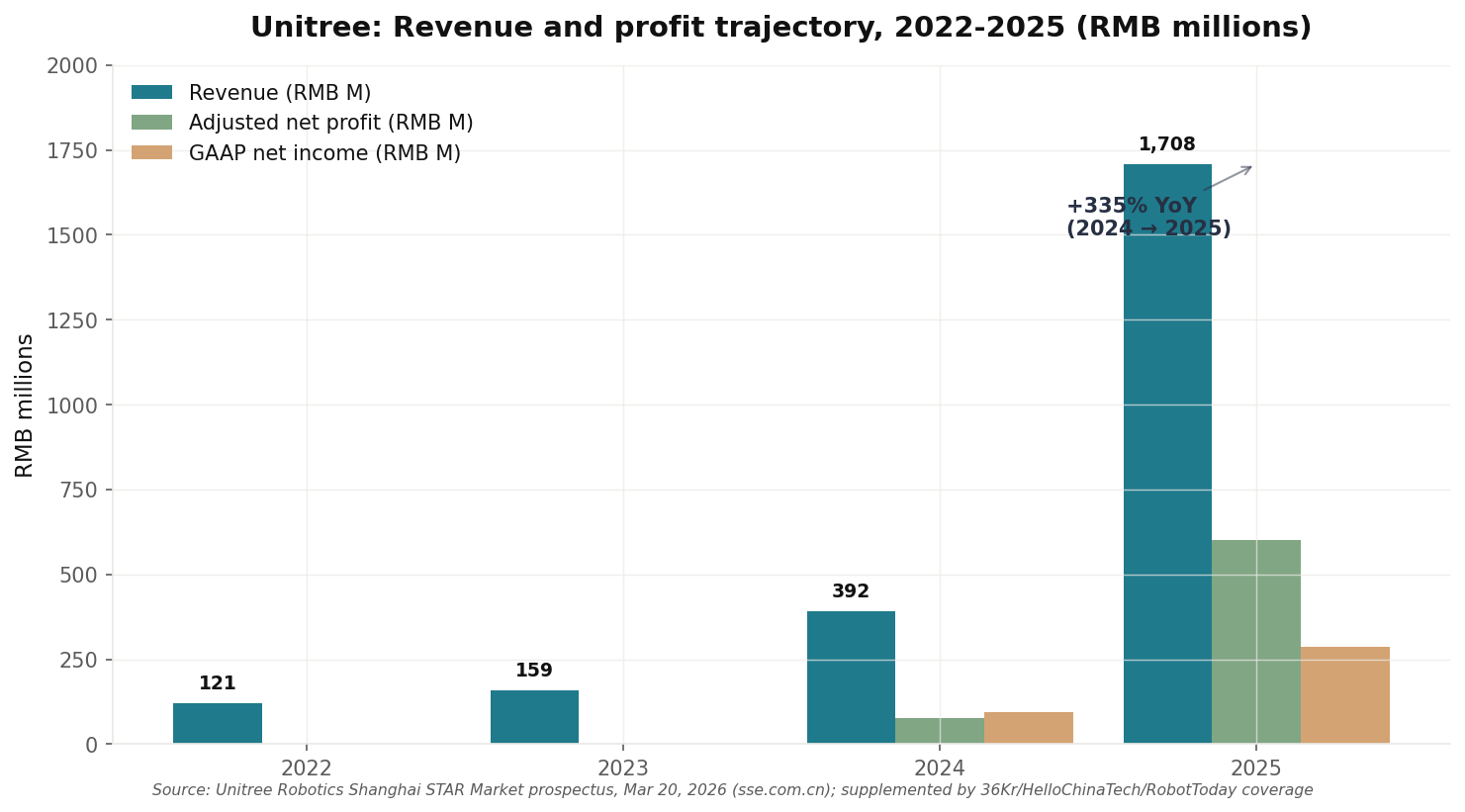

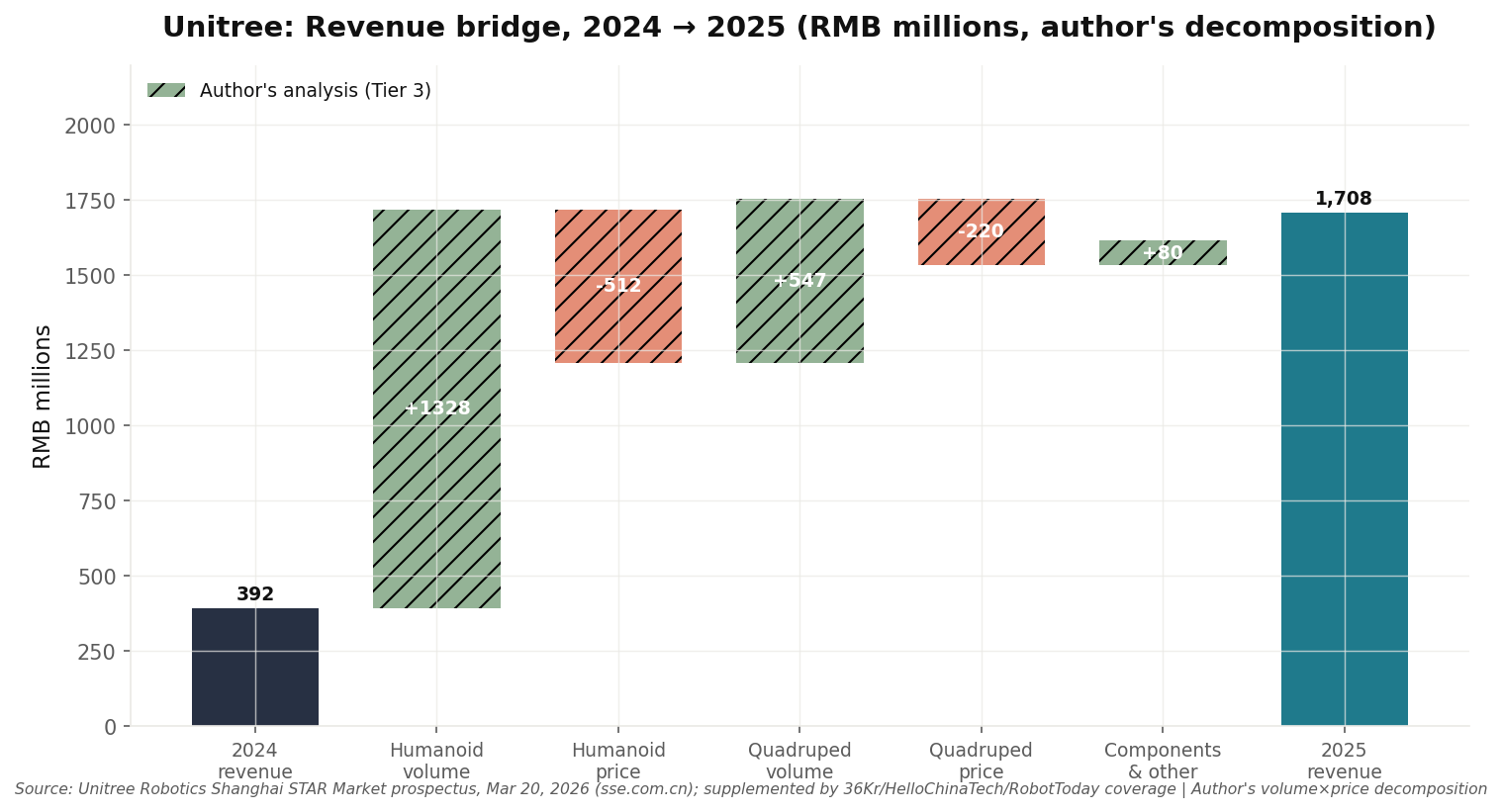

On March 20, 2026, Unitree filed a 363-page prospectus seeking ¥4.2 billion (~$610 million) [10][11][12][14]. 2025 revenue was ¥1.71 billion, up 335% year-on-year from ¥392 million in 2024. Adjusted net profit was ¥600 million, a 674.3% increase. Gross margin reached approximately 60% [10][13][15]. Unitree shipped over 5,500 humanoid units in 2025, taking 32.4% of the global humanoid market by units [11][13]. The average selling price of a Unitree humanoid fell from ¥593,400 in 2023 to ¥167,600 in 2025, a 72% drop in two years, even as gross margin improved [10][13].

The prospectus also disclosed that Unitree designs and assembles most components in-house, with purchased parts running roughly 14–18% of total cost. Per-unit cost on quadrupeds had fallen from ¥22,300 in 2022 to ¥12,100 in the first nine months of 2025; humanoid unit cost had fallen from ¥73,200 to ¥62,200 over the same window [13][15].

The open question now is the brain. Unitree’s hardware lead is real, durable, and difficult to replicate without replicating nine years of motor design. But hardware is not what humanoid customers are waiting on. Wang himself, speaking at the 2025 World Robot Conference, was direct. Current robot hardware is sufficient; embodied AI is inadequate; the field is roughly at the pre-ChatGPT stage; the breakthrough is somewhere between two and five years out [33].

I believe that embodied intelligence is the only path to achieving AGI. Currently, LLMs lack physical presence and thus have an insufficient understanding of the physical world. AGI is very likely to emerge from robotics companies.

Wang Xingxing, panel remarks, 2024, cited in ChinaTalk [33]

The 50-times-revenue valuation that the IPO assumes prices in a future in which Unitree’s hardware moat extends into the embodied-AI moat. There is no guarantee it will.

Active learning question. You are pricing the Unitree IPO. The company’s hardware is the cheapest and best-shipped in the world; its software is several years behind frontier embodied-AI labs; its US revenue is geopolitically constrained. Do you anchor your valuation on (a) the multiple of a hardware leader like SMIC or Hikvision, (b) a category-creating tech leader like Tesla or NVIDIA, or (c) something in between? What would have to be true in 2027 for the bet to work?

Cross-Industry Parallels

Unitree’s trajectory rhymes with earlier hardware stories.

BYD. Like Unitree, BYD started in low-end components (batteries first, then EV powertrains) and spent fifteen years building vertical integration into chemistry and pack design before the category arrived. When Tesla globalized the electric-car narrative around 2018, BYD already had a cost structure that no Western incumbent could match. The pattern is identical to what Unitree did between 2017 and 2023. They spent a decade making the cheapest version of a not-yet-popular product, then rode the surrounding category into a category leadership position.

Honda’s CVCC engine in the early 1970s. Faced with US Big Three incumbents who saw small fuel-efficient cars as a side market, Honda, then a motorcycle company, spent five years engineering a stratified-charge gasoline engine that met the 1970 US Clean Air Act emissions standards without a catalytic converter. The CVCC was not the most powerful engine in the world. It was the cheapest engine that met the new rules. By 1975, Honda had Civic sales the Big Three couldn’t match in their own market. Unitree’s H1 in 2023 plays the same role. It is not the most capable humanoid; it is the first one that an academic lab in Stuttgart, Tsinghua, or Carnegie Mellon could actually buy this quarter on a research budget.

Lessons

Vertical integration in young hardware markets compounds in ways that financial models almost always undercount. Unitree spent six years before the Go1 designing its own motors and reducers because off-the-shelf components were too expensive and slow to procure. That decision looked like a cost choice in 2018; by 2023 it was the only reason Unitree could ship a humanoid for $16,000 while every Western competitor’s bill of materials still ran above $50,000. Hardware moats look like cost decisions until they become category decisions.

Selling pickaxes during the prospecting phase funds the gold-rush bet. From 2017 through 2022 Unitree was effectively a research-instrument company, selling quadrupeds to PhD labs that paid in cash and never returned the product. That cash-flow loop (small ticket, repeat customer, high gross margin) funded the R&D that produced the H1 humanoid in six months once Wang decided the timing was right in 2023. A company that had taken government and military contracts instead would have been locked into a single buyer’s roadmap.

Cheap-but-credible beats expensive-and-perfect in markets that do not yet exist. Boston Dynamics has shipped more capable robots than Unitree at every product comparison since 2017. Almost no academic robotics paper published since 2022 uses a Boston Dynamics platform; almost all of them use a Unitree. The category went to whoever the next thousand researchers could afford. When you don’t know what the killer use case is, the company that captures the experimentation surface wins by default.

Cost-as-the-only-KPI works until intelligence becomes the moat, and Unitree has not yet proven it can survive that transition. The company’s R&D spend on embodied AI was a rounding error until 2024 and only grew exponentially in 2025. The 50-times-revenue valuation in the IPO assumes that the hardware lead translates into an AI lead. If it doesn’t, Unitree becomes the foundry, making bodies for somebody else’s brains. The bet on the IPO is implicitly that Wang’s culture of cost discipline is also a culture that can pivot to model-training spend at order-of-magnitude scale, and the historical evidence on that is thin.

The CloudSail and UniPwn vulnerabilities reveal a strategic blind spot that the cost culture itself produced. Shipping research-grade firmware at the scale of US prisons and Army installations turned a small engineering choice (cheap, undocumented remote-access tunnels and default credentials) into a bipartisan US Congressional cause, with concrete consequences for export market access. In hardware companies that scale into critical-infrastructure customers, security is not a feature you can defer, because the cost of being wrong stops being measured in dollars and starts being measured in entity-list designations. Unitree’s biggest unforced error in its first decade was not technical; it was failing to match its security posture to the reach of its product. The company is still paying for that.

Part II: Financial Deep-Dive

Promised vs Delivered

Unitree management has been an operational deliverer with a slipping AI timeline.

Unitree delivers on hardware milestones — products, prices, manufacturing scale — and underdelivers on AI and capital-markets timelines. This matters for the IPO because the bull case requires AI-leader execution, not hardware execution, and the historical track record on AI is one missed prediction (general-purpose model by end-2025) plus two security disclosures the company underestimated.

Lens 1: Historical Performance

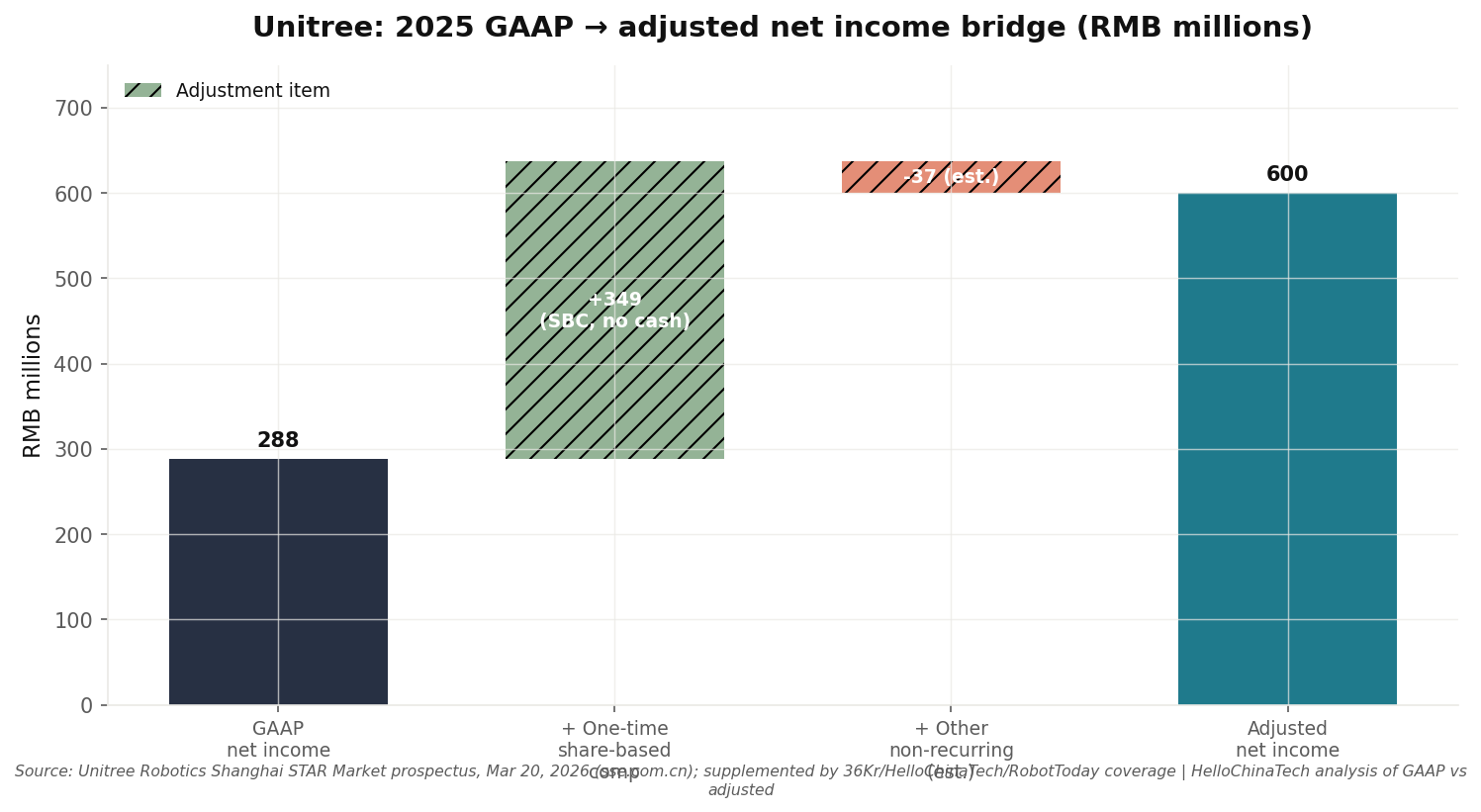

Unitree turned cash-flow positive in 2020 by company disclosure [6], but GAAP profitability arrived only in 2024 with RMB 94.5M net income on RMB 392M revenue (24% margin) [46]. 2025 GAAP net income reached RMB 288M; adjusted net income, which strips out a one-time RMB 349M share-based compensation charge tied to an employee equity incentive program, was RMB 600M (35% margin on revenue) [15][46]. Operating cash flow in 2025 reached RMB 672M, materially higher than GAAP net income [15][46] — a positive QoE signal that the underlying business is genuinely cash-generating, not just accounting-profitable.

Lens 2: Growth Anatomy

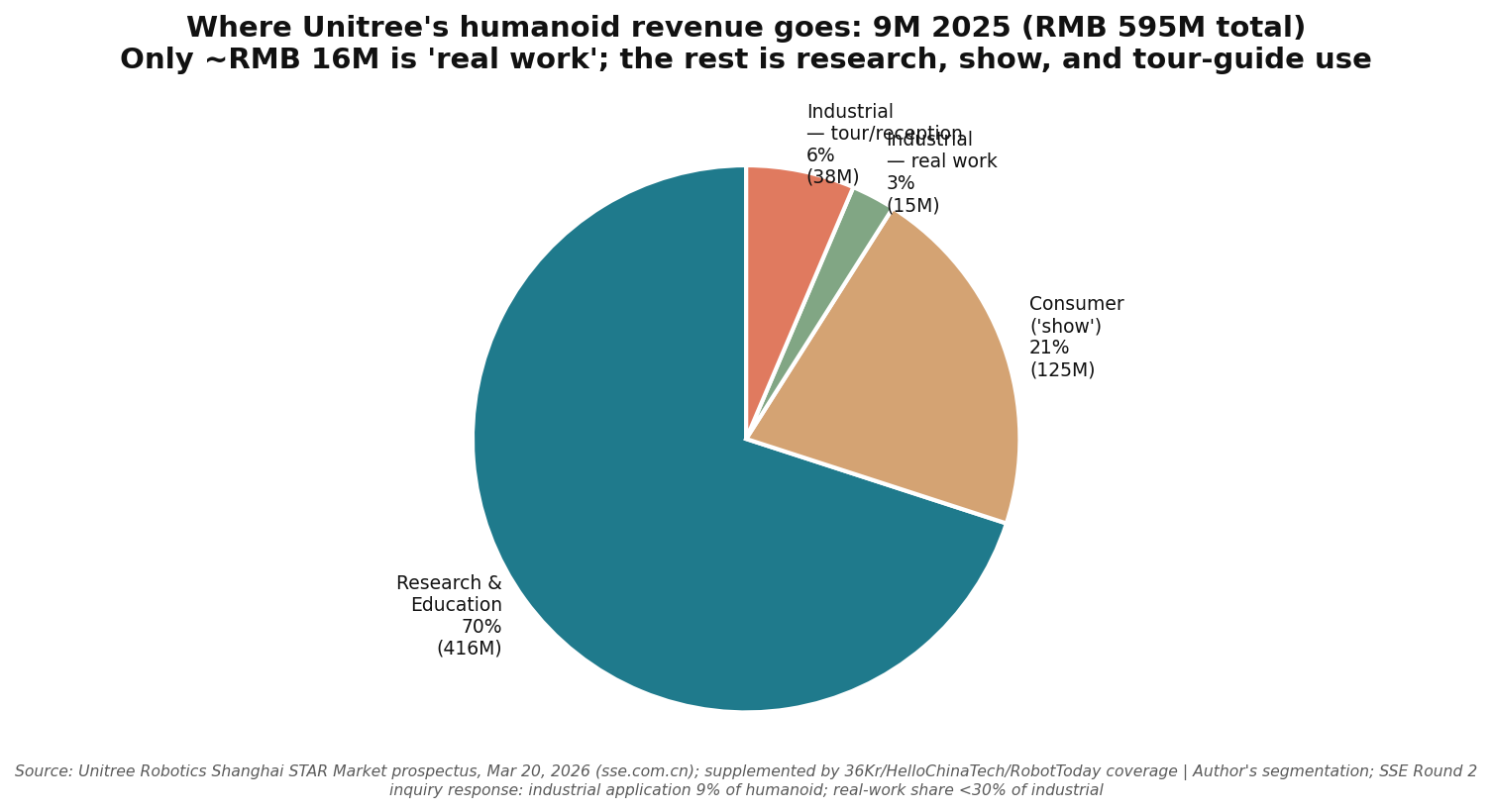

Real growth is coming from 2025 volume-elasticity at substantially lower humanoid prices, in domestic Chinese channels, on a customer base that is still ~70% Research-and-Education. Whether that growth is durable depends on whether industrial customers convert from “tour guide” deployments to “real work” deployments — and the prospectus discloses that as of 9M 2025, real-work industrial revenue was just RMB 15.7M [15][46].

Lens 3: Unit Economics Architecture

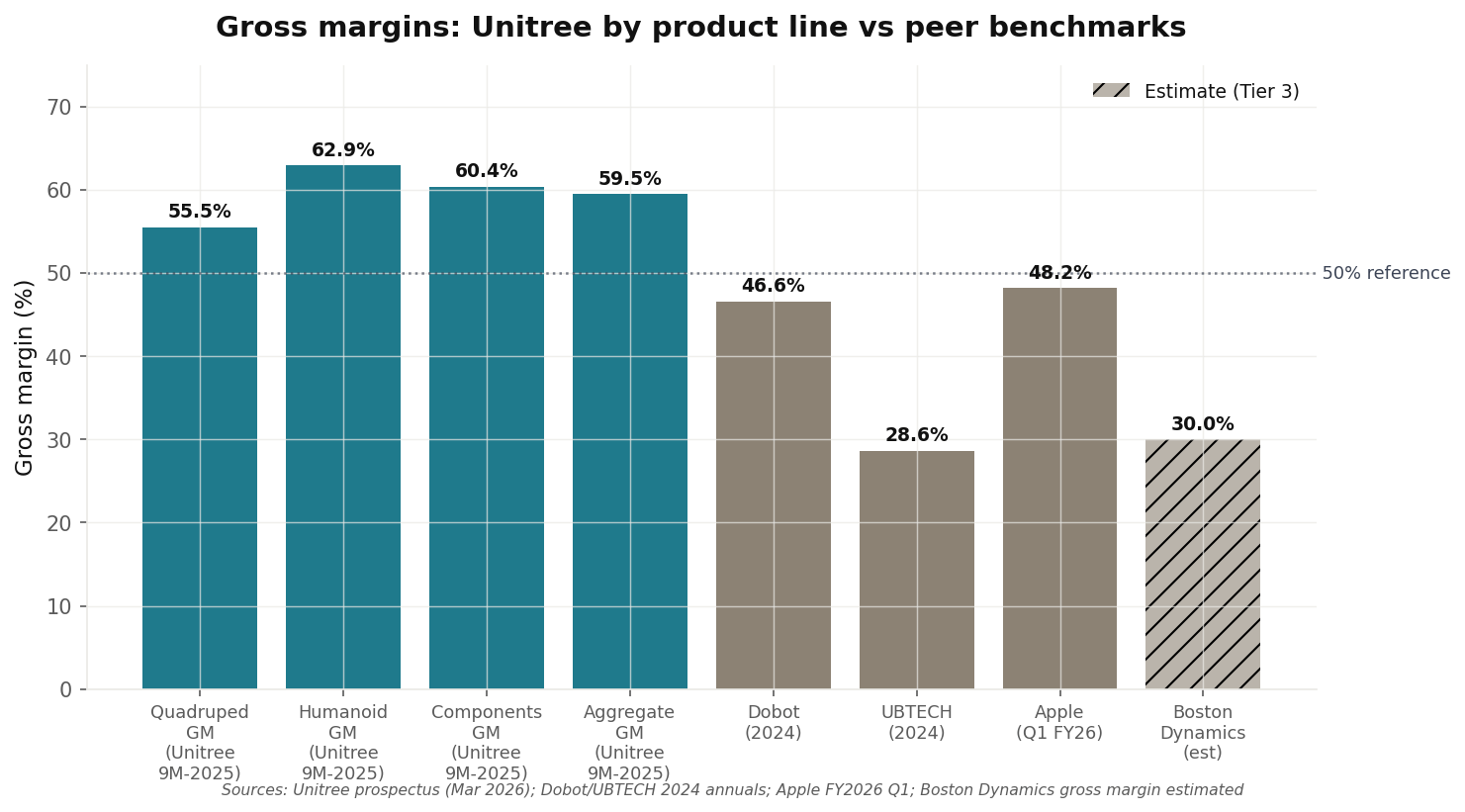

Quadruped robots: 55.5% gross margin. Quadruped ASP was RMB 27,200 in 9M 2025; per-unit cost RMB 12,100. Gross profit per quadruped: RMB 15,100 [46].

Humanoid robots: 62.9% gross margin. Humanoid ASP RMB 167,600; per-unit cost RMB 62,200. Gross profit per humanoid: RMB 105,400 [13][46]. Note: humanoid GM was 87.7% in 2023 (5 H1 units sold at RMB 593,400) and has compressed as the product mix shifted to mass-market G1 — but the cost base also fell.

Components: 60.4% gross margin. Roughly RMB 60M revenue in 9M 2025; high gross profit reflects supply-side pricing power — Unitree sells motors and dexterous hands to other Chinese robotics companies [46][49].

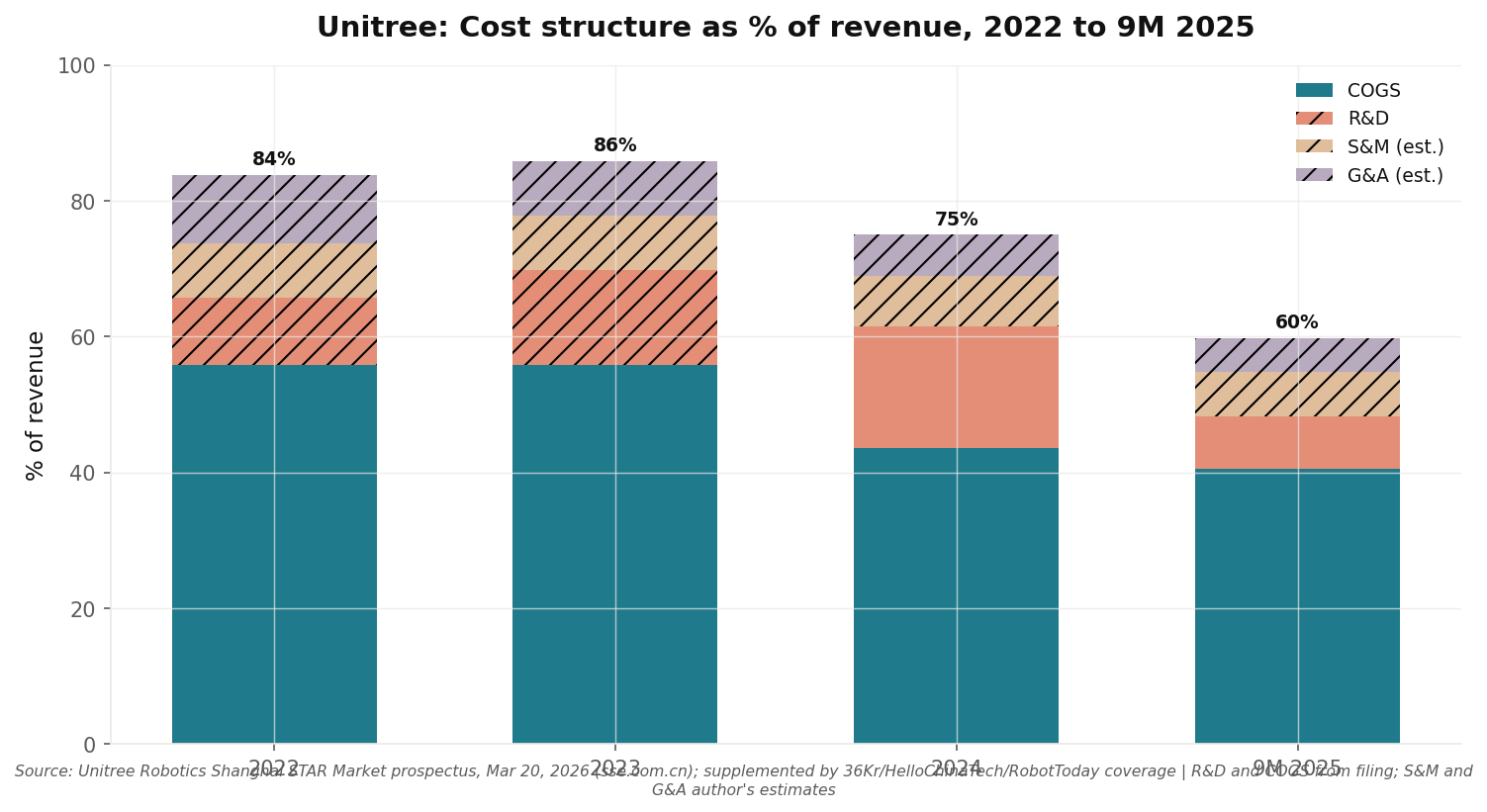

Lens 4: Cost Structure & Operating Leverage

Unitree’s scale economics have come almost entirely from R&D operating leverage and procurement scale on a tiny team. The next leg of operating leverage requires the manufacturing facility — which will hurt margins on the way up before it helps them.

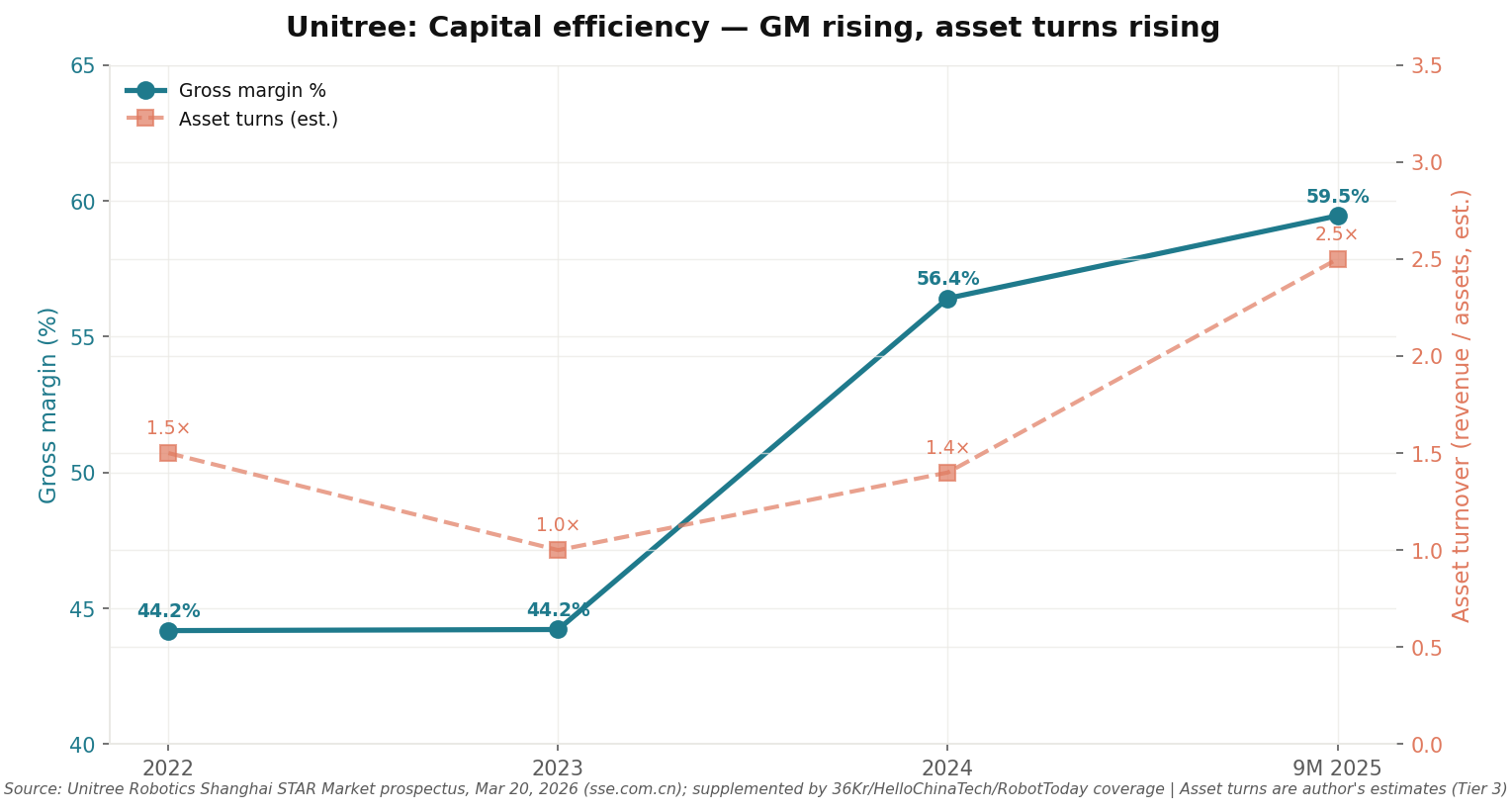

Lens 5: Capital Efficiency & Cash Conversion

This is a research-grade result for a hardware company. The driver is the combination of unusually high gross and operating margins (above) with a small invested capital base (no owned real estate before the planned Hangzhou facility, lean working capital tied to a sell-through rate of 86% on quadrupeds and 96% on humanoids [46][51] — meaning Unitree produces almost exactly what it sells, with minimal inventory tie-up). Chinese coverage has noted the company’s monthly sales-production-procurement coordination meeting as the operating mechanism for this discipline [48][51].

Unitree is the rare profitable robotics company because its hardware-side capital intensity has been kept artificially low through asset-light contract manufacturing and aggressive procurement. That low intensity is by design but is also fragile — it ends with the IPO.

Lens 6: Customer Cohort Economics

Unitree’s most reliable customers buy robots they don’t put to productive work. The bull case requires industrial customers — exactly the customers whose buying behavior Unitree has acknowledged it does not fully understand [15][46].

Lens 7: Competitive Position (7 Powers)

Applying Hamilton Helmer’s 7 Powers framework to Unitree:

Scale Economies — Yes, hardware-side. Unitree’s per-unit cost on quadrupeds fell 46% from 2022 to 9M 2025; humanoid per-unit cost fell 15% from 2024 to 2025 [46]. The mechanism is purchasing scale on shared components across product lines plus learning-curve effects on motor and reducer manufacturing. This is a real and currently widening moat against any new entrant building from scratch.

Network Economies — Weak. Robots do not benefit much from network effects in the way platforms do. The closest analog is the developer ecosystem around Unitree’s open SDK, ROS support, and (more recently) the open-source UnifoLM model [9]. This generates ecosystem stickiness with academic users but not the kind of compounding that Helmer’s framework treats as a “power.”

Counter-positioning — Yes, against Boston Dynamics specifically. Unitree’s commitment to electric drives, low-cost motors, and academic-priced units is structurally incompatible with Boston Dynamics’ hydraulic-and-premium business model. Boston Dynamics, owned by Hyundai since 2020, cannot easily cannibalize its $74,000 Spot price point [21] without imploding its existing customer base. Wang explicitly noted in the April 2024 TMTPost interview that he had assumed Boston Dynamics would have moved to electric drive years earlier and was surprised when they did not [18].

Switching Costs — Weak in academia, stronger in industrial. Academic customers integrate Unitree robots into research workflows; switching to UBTECH or Boston Dynamics requires re-validating algorithms and re-writing integration code. State Grid’s quadruped inspection deployments have higher switching costs because the robot is integrated into substation operations [49]. Humanoid switching costs are essentially zero today because no humanoid is doing useful work at any meaningful scale.

Branding — Significant in China, growing globally. The Spring Festival Gala plus the Xi Jinping symposium plus the Time 100 Most Influential People listing for Wang in 2025 [9][34] gave Unitree the strongest robotics brand in China. Globally, the brand is recognizable in robotics but has been damaged by the bipartisan US Congressional letter and the security disclosures [26][28].

Cornered Resource — Partial. Wang Xingxing himself is something close to a cornered resource: his combination of cost obsession, hardware judgment, and willingness to operate inside Chinese government priorities is rare. The 150+ patents Unitree has filed since 2018 are a softer cornered resource. Component supply (high-torque motors, harmonic reducers) is not a cornered resource — it is increasingly commoditized in the Yangtze River Delta [42].

Process Power — Partial. Six to seven years of motor iteration is process power [21]. Sub-30-day inventory days is process power. The monthly sales-production-procurement coordination meeting is process power [48]. This is real but invisible to investors.

Unitree has 2-3 of Helmer’s 7 Powers — Scale Economies in hardware, Counter-positioning against Boston Dynamics, and Branding in China. Those three are durable for 24-36 months. None of them transfer cleanly to the embodied-AI competition that defines the next 5 years.

Lens 8: Capital Allocation Track Record

Unitree’s capital allocation history through May 2026 is short and disciplined. There has been no M&A — every product Unitree sells was developed in-house. There has been no debt of consequence. The company has raised approximately RMB 700-800M cumulatively in cash through 11 funding rounds [18][39][42], against a cumulative R&D investment of approximately RMB 350M and a cumulative net profit (2024-2025) of approximately RMB 380M [9][46].

Wang has been one of the most disciplined capital allocators in Chinese hard tech. The IPO is the first time he is committing serious capital to a category (embodied-AI models) where his historical advantages do not transfer.

Lens 9: Quality of Earnings

Unitree’s reported earnings are substantially clean. The RMB 349M SBC adjustment is large but defensible as one-time. The bigger issue is what isn’t disclosed — segment-level operating economics and customer concentration are gaps that an audited 2026 H1 filing should close.

Citations

[1] “Unitree Robotics,” Wikipedia, accessed May 2026. https://en.wikipedia.org/wiki/Unitree_Robotics

[2] “Wang Xingxing,” Wikipedia, accessed May 2026. https://en.wikipedia.org/wiki/Wang_Xingxing

[3] “Unitree founder Wang Xingxing: A post-90s robotics genius,” Our China Story, March 2025. https://www.ourchinastory.com/en/14416/Unitree-founder-Wang-Xingxing:-A-post-90s-

[4] Mike Kalil, “The Rise of Wang XingXing’s Unitree Robotics,” Mike Kalil Blog, November 2025. https://mikekalil.com/blog/rise-of-unitree/

[5] “Wang Xingxing (王兴兴),” The Wire China, September 2025. https://www.thewirechina.com/whos_who/wang-xingxing-%E7%8E%8B%E5%85%B4%E5%85%B4/

[6] “From Robot Dogs to Humanoids: The Unlikely Rise of Unitree Robotics,” Pandaily, June 2025. https://pro.pandaily.com/p/from-robot-dogs-to-humanoids-the

[7] “Meet Wang Xingxing, the young Chinese robotics star from Unitree at Xi Jinping’s symposium,” South China Morning Post, February 2025. https://www.scmp.com/tech/big-tech/article/3299435/meet-wang-xingxing-young-chinese-robotics-star-unitree-xi-jinpings-symposium

[8] Wang Xingxing profile, Baidu Baike (English), accessed May 2026. https://baike.baidu.com/en/item/Wang%20Xingxing/13316

[9] Irene Zhang, “Unitree Goes Public,” ChinaTalk, April 2026. https://www.chinatalk.media/p/unitrees-ipo

[10] Zeyi Yang, “China robot maker Unitree files for $610 million Shanghai IPO,” Rest of World, March 2026. https://restofworld.org/2026/unitree-china-humanoid-robot-shanghai-ipo/

[11] “China’s Unitree Robotics rides humanoid tide as it targets US$610m IPO,” South China Morning Post, March 2026. https://www.scmp.com/business/banking-finance/article/3347365/chinas-unitree-robotics-rides-humanoid-tide-it-targets-us610m-ipo

[12] “China’s Unitree Robotics Files for $610 Million Shanghai IPO to Fund AI,” Bloomberg, March 2026. https://www.bloomberg.com/news/articles/2026-03-20/chinese-robot-maker-unitree-seeks-610-million-in-shanghai-ipo

[13] “Humanoid Robots Go Public: China’s Unitree Files $610M IPO Amid Surging Demand,” eWeek, April 2026. https://www.eweek.com/news/unitree-robotics-ipo-humanoid-robots-profitability-china/

[14] “China’s Unitree Robotics Files for USD608 Million IPO in Shanghai,” Yicai Global, March 2026. https://www.yicaiglobal.com/news/chinas-unitree-robotics-to-raise-usd608-million-in-shanghai-star-market-ipo

[15] Poe Zhao, “Unitree’s $610M IPO Shows What Humanoid Robotics Really Sells,” HelloChinaTech, March 2026. https://hellochinatech.com/p/unitree-ipo-humanoid-robotics-really-sells

[16] “Unitree plans Shanghai IPO, testing interest in humanoid robots,” CNBC, March 2026. https://www.cnbc.com/2026/03/20/unitree-plans-shanghai-ipo-testing-interest-in-humanoid-robots.html

[17] “Unitree’s Shanghai listing tests Boston Dynamics: boom or bubble?,” The Korea Herald (The Investor), March 2026. https://www.theinvestor.co.kr/article/10705814

[18] “Exclusive: Unitree Robotics Founder Says General-Purpose Large Models for Robots Will be Achieved by Yearend,” AsianFin / TMTPost, February 2025. https://en.tmtpost.com/post/7460993

[19] Brianna Wessling, “Unitree becomes a legged robot unicorn with Series C funding,” The Robot Report, June 2025. https://www.therobotreport.com/unitree-becomes-a-legged-robot-unicorn-with-series-c-funding/

[20] Susanne Tang, “Introducing Unitree, China’s leading AI-embodied Robotics Company,” AIProem, February 2025. https://aiproem.substack.com/p/introducing-unitree-chinas-leading

[21] Evan Ackerman, “Unitree’s Go1 Robot Dog Looks Pretty Great, Costs Just USD $2700,” IEEE Spectrum, June 2021. https://spectrum.ieee.org/unitrees-go1-robot-dog-looks-pretty-great-costs-just-usd-2700

[22] “Unitree Robotics,” Robots Guide / IEEE Spectrum, August 2025. https://robotsguide.com/robots/unitree-h1

[23] “Tradition meets tech: Unitree robots dance at Spring Festival Gala,” CGTN, January 2025. https://news.cgtn.com/news/2025-01-28/Tradition-meets-tech-Unitree-robots-dance-at-Spring-Festival-Gala-1Axm5TuIAve/index.html

[24] “China’s Spring Festival Gala shows off AI, cloud computing, humanoid robots,” CGTN, January 2025. https://news.cgtn.com/news/2025-01-29/China-s-Spring-Festival-Gala-incorporates-cloud-computing-1AyUGAHIZsQ/p.html

[25] “Humanoid robots dance to folk tunes on China’s New Year Gala,” Interesting Engineering, January 2025. https://interestingengineering.com/innovation/humanoid-robots-dance-chinas-new-year

[26] “Trojan Horse Tech: Select Committee Sounds Alarm on CCP Robots Inside U.S. Institutions,” US House Select Committee on the CCP, May 2025. https://chinaselectcommittee.house.gov/media/press-releases/trojan-horse-tech-select-committee-sounds-alarm-on-ccp-robots-inside-us-institutions

[27] Letter to Secretary of Defense Pete Hegseth et al., US House Select Committee on the CCP, May 6, 2025. https://chinaselectcommittee.house.gov/sites/evo-subsites/selectcommitteeontheccp.house.gov/files/evo-media-document/Unitree.pdf

[28] Evan Ackerman, “Security Flaw Turns Unitree Robots Into Botnets,” IEEE Spectrum, October-December 2025. https://spectrum.ieee.org/unitree-robot-exploit

[29] Sam Sabin, “Chinese robotics manufacturer left backdoor in product,” Axios, April 2025. https://www.axios.com/2025/04/01/threat-spotlight-backdoor-in-chinese-robots-future-of-cybersecurity

[30] “Who’s Snooping on Go1 Robot Dogs?,” Centraleyes, April 2025. https://www.centraleyes.com/whos-snooping-on-go1-robot-dogs/

[31] “Hidden ‘doggy door’ found in Chinese-made robot dogs,” Field Effect, April 2025. https://fieldeffect.com/blog/hidden-doggy-door-robot-dogs

[32] “CVE-2025-35027: Multiple robotic products by Unitree…,” CVE Details, September 2025. https://www.cvedetails.com/cve/CVE-2025-35027/

[33] “Unitree CEO on China’s Robot Revolution,” ChinaTalk (translation of Titanium Media interview), March 2025. https://www.chinatalk.media/p/unitree-ceo-on-chinas-robot-revolution

[34] Lily Ottinger, “Xi’s Hard Tech Avengers,” ChinaTalk, February 2025. https://www.chinatalk.media/p/xis-hard-tech-avengers

[35] “Zhi Huijun and Wang Xingxing Engage in a Crucial Battle in the Humanoid Robot Field,” 36Kr, 2025. https://eu.36kr.com/en/p/3373006296979845

[36] “Post-90s Member Wang Xingxing Challenges IPO with a Robot Adventure Valued Over 12 Billion Yuan,” 36Kr, September 2025. https://eu.36kr.com/en/p/3456193708791168

[37] “Unitree Technology Completes Nearly 700M Yuan Series C Financing with Tencent, Alibaba, China Mobile as Investors,” 36Kr, June 2025. https://eu.36kr.com/en/p/3344368397190018

[38] “Unitree IPO Profile: $7B Valuation, Pre-IPO 2026,” Tech Market Briefs, April 2026. https://techmarketbriefs.com/pre-ipo/unitree/

[39] “Unitree: 2026 Funding Rounds & List of Investors,” Tracxn, March 2026. https://tracxn.com/d/companies/unitree/__o1e8b3ZlyUCcjIECfbM9csfhnJyv1_fOku8o_K8gCYg/funding-and-investors

[40] “In the robot highland where many strong people gather, how did Wang Xingxing’s Yu Shu stand out?,” iNews, 2025. https://inf.news/en/tech/ab94455c29cc6cae28dee1000c805160.html

[41] “Wang Xingxing and Jun Zhihui Compete for the First Place,” 36Kr, October 2025. https://eu.36kr.com/en/p/3508701431208839

[42] “Half of the Investment Circle Owes Gratitude to Unitree,” 36Kr, March 2026. https://eu.36kr.com/en/p/3732145162944770

[43] “Unitree founder Wang Xingxing to People’s Daily,” Global Times, August 2025. https://www.globaltimes.cn/page/202508/1340752.shtml

[44] “Unitree Robotics CEO on AI-driven humanoid robot evolution,” CGTN, February 2025. https://news.cgtn.com/news/2025-02-19/Unitree-Robotics-CEO-on-AI-driven-humanoid-robot-evolution-1B7IABSmmVa/p.html

[45] “Unitree Goes Public” / Power chart of Unitree’s R&D growth, ChinaTalk, April 2026. https://www.chinatalk.media/p/unitrees-ipo

[46] Unitree Robotics Shanghai STAR Market prospectus, March 20, 2026. https://static.sse.com.cn/stock/disclosure/announcement/c/202603/002178_20260320_QY8F.pdf

[47] “What is the secret behind Unitree’s high gross margins?” KrAsia (translated 36Kr), March 2026. https://kr-asia.com/what-is-the-secret-behind-unitrees-high-gross-margins

[48] “Unveiling the Secret Behind Unitree’s 60% Gross Profit Margin,” 36Kr, March 2026. https://eu.36kr.com/en/p/3735272591212546

[49] “We’ve All Misjudged Unitree: Telling Humanoid Robot Stories, Making Money from Robotic Dogs,” 36Kr, April 2026. https://eu.36kr.com/en/p/3750758796898825

[50] “Unitree Profits, but Humanoid Robots Fail to Make Money,” 36Kr, March 2026. https://eu.36kr.com/en/p/3735276262601477

[51] “Digging Deep into Unitree’s Prospectus,” 36Kr, March 2026. https://eu.36kr.com/en/p/3731404085015046

[52] “Unitree Robotics IPO Reaches Key Milestone,” Gasgoo, March 2026. https://autonews.gasgoo.com/articles/market-industry/unitree-robotics-ipo-reaches-key-milestone-2036052042919866369

[53] “Unitree Robotics Files IPO,” RobotToday, March 2026. https://robottoday.com/article/unitree-robotics-files-ipo-china-s-humanoid-robot-leader-targets-42-b-valuation

[54] “Unitree Earns 600M Yuan, UBTECH Loses 700M,” 36Kr, April 2026. https://eu.36kr.com/en/p/3780412419502851

[55] UBTECH Robotics 2024 Annual Report and 2025 Interim Report, www.ubtrobot.com Investor Relations

[56] UBTECH Robotics earnings release, March 31, 2026, TradingView. https://www.tradingview.com/news/urn:summary_document_report:quartr.com:3215684:0-ubtech-robotics-corp-industrial-humanoid-robot-sales-soared-driving-revenue-up-53-and-sharply-reducing-net-loss/

[57] “Figure Exceeds $1B in Series C Funding at $39B Post-Money Valuation,” PR Newswire, September 2025. https://www.prnewswire.com/news-releases/figure-exceeds-1b-in-series-c-funding-at-39b-post-money-valuation-302556936.html

[58] “Figure AI valuation, funding & news,” Sacra, accessed May 2026. https://sacra.com/c/figure-ai/

[59] “Boston Dynamics: Shift from Hydraulic to Electric Actuation: A New Era in Robotics,” CubeMars, May 2024. https://www.cubemars.com/article-303-Boston+DynamicsShift+from+Hydraulic+to+Electric+Actuation+A+New+Era+in+Robotics.html

[60] “Boston Dynamics,” Wikipedia, accessed May 2026. https://en.wikipedia.org/wiki/Boston_Dynamics

[61] “Boston Dynamics Atlas: The Agile Humanoid Robot Pioneer,” BotInfo.ai, accessed May 2026. https://botinfo.ai/articles/boston-dynamics-atlas

[62] “First Principles: The Mechanics of Humanoid Robots,” Hardware FYI Substack, June 2024.

[63] “GO Motor — Bionic Robot Joint Motor,” Unitree Robotics product page, accessed May 2026. https://www.unitree.com/mobile/go1/motor/

[64] “GO-M8010-6 Motor,” Unitree Shop product page, accessed May 2026. https://shop.unitree.com/products/go1-motor

[65] “A1 Motor — Stable and Efficient with Hardcore Strength,” Unitree Robotics product page, accessed May 2026. https://www.unitree.com/mobile/a1/motor/

[66] “Unitree Robotics Go1 Pro,” Wevolver specifications page, accessed May 2026. https://www.wevolver.com/specs/unitree-robotics-go1-pro